Fiat Currency Lifespans and Bitcoin: A Warning for Risk Assets

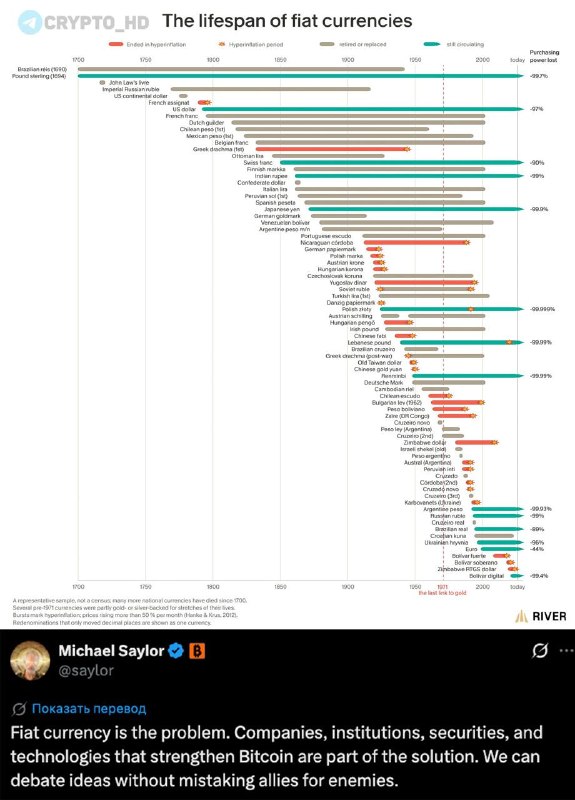

A chart from River puts the average lifespan of a fiat currency at 27 years. Many currencies in its dataset disappeared after hyperinflation or were replaced. That raises an awkward question: how dependable is the unit used to price everything in a portfolio? My take: investors should not brush that aside. For Bitcoin supporters, the chart strengthens the case for keeping some wealth outside the sovereign currency system.

The data goes back to 1700, and the record is rough. Fiat currencies have finite lives. Many disappeared. Some survivors lost between 90% and 99.9% of their purchasing power. The damage hides in plain sight because it often unfolds slowly: an account balance grows, yet the money buys less each year. Wait a decade or two. Then it shows. Michael Saylor calls fiat “the problem.” I’ll be honest: that phrase is too neat for a complicated subject. Still, while one chart cannot prove that every fiat system will collapse, it does document how often currencies fail, get replaced, or lose value over time.

This history feeds into the macro flow case heard across crypto markets. Central banks are still wrestling with inflation, and 2022 remains fresh in investors’ minds. Inflation fears moved some capital into supposed hedges such as Bitcoin (BTC), even as the NASDAQ 100 struggled during parts of the first quarter. The strategy was messy. These trades usually are. Most bullish accounts stop there. That’s only half right. When the Federal Reserve raised rates aggressively, BTC plunged from nearly $69,000 to roughly $15,500. Why does this matter? Because the collapse showed, painfully, that Bitcoin still behaves like a risk asset when liquidity disappears. Yet the longer-term concern remains. Investors looking beyond the next rate decision may see Bitcoin’s fixed supply as protection against decades of currency debasement—not merely a wager on whether inflation reaches 2% this year.

Fiat’s history also lends some support to Bitcoin’s possible role as a safe haven during financial stress. Gold has filled that role for generations. Bitcoin is different: it is digital and can cross borders. It is also hard for any single government to control. There are hints of crisis demand, but the evidence is nowhere near settled. After the Soleimani strike in January 2020, BTC gained about 8% within 72 hours. I wouldn’t build the whole case on that move. It is worth noticing, but it does not establish Bitcoin as a safe haven—especially since the asset has also fallen hard during market panics. Counter to the usual pitch, scarcity alone does not guarantee stability. Even so, River’s chart gives investors a concrete reason to ask whether a future economic or geopolitical shock could push more money beyond national currency systems.

Some Bitcoin advocates call companies and institutions that support the network “part of the solution.” The slogan is a little grandiose, in my view, but it conceals a legitimate investment thesis: buying Bitcoin, or shares in businesses with heavy exposure to it, is a bet that fiat erosion will continue. Selectivity still matters. A corporate treasury can hold Bitcoin while the underlying company remains financially unhealthy. Friendly language does not make every crypto project trustworthy, either. Look at the balance sheet and custody arrangements first. Then examine debt, fees, and management. Quite a lot, actually.

What this means

The history of failed and short-lived currencies changes the calculation around long-term wealth protection. Bitcoin remains speculative, but some investors now use it as insurance against weakening sovereign money. MicroStrategy’s large BTC purchases are the most visible corporate example. Spot Bitcoin ETFs give institutions a more familiar route into the asset. Are those buyers only chasing returns? Probably not all of them. Some may also be trying to protect purchasing power over several decades. Fiat currencies have an uneven record there. BTC is the ticker most directly affected because its scarcity case grows stronger whenever trust in fiat slips. That case isn’t foolproof.

Inflation reports and central bank decisions are the next things to watch. If inflation rises for a sustained period across major economies, demand for Bitcoin as a hedge could return. FOMC meetings matter as well. Lower rates or easier policy have often helped risk assets, including BTC, though the pattern can break when markets are scared enough. Yes, that complicates the hedge argument. It should. Spot Bitcoin ETF flows offer a cleaner reality check, particularly when read alongside daily trading volume. A large and persistent increase would show that bigger investors are committing money to the fiat-debasement thesis instead of merely discussing it.

The price level to watch is $70,000. A convincing break above that resistance could bring buyers back and restart bullish momentum. Simple enough. Price still cannot explain why those buyers arrived. Some may be worried about currency erosion; others may just be chasing a breakout. Both groups can lift BTC for a time. Once momentum fades, however, the difference matters.