EXMO Pulls the Plug: Sanctions Force Exchange Wind-Down, Users Get IOU Tokens

EXMO.com is shutting down after UK financial sanctions struck companies in its group. User balances have been cut by 29.4%, with the missing funds replaced by non-tradable USDRecover (USDRec) IOU tokens. Put plainly, customers are missing almost one dollar for every three they were owed. It happened fast. My take: this is less a story about crypto prices than about what happens when someone else holds your assets.

EXMO announced an orderly wind-down after the UK’s Foreign, Commonwealth and Development Office added EXMO Exchange Limited to its Russia sanctions list on May 26, 2026. The exchange disputes the decision but says it is cooperating. The designation formed part of a package targeting the “A7 network,” which UK officials accused of supplying crypto and banking infrastructure to Russia’s war economy. Officials also named HTX, formerly Huobi. Bitpapa and Rapira Group were included too. EXMO had long been popular among Russian-speaking traders.

EXMO says it left Russia after the 2022 invasion of Ukraine, when it sold its Russian business to a rebranded company called Exmo.me. TRM Labs later questioned whether the separation was complete: on-chain records, the blockchain analytics firm said, showed EXMO and Exmo.me continuing to share custodial wallet infrastructure after the sale. That link probably played a part in the UK’s decision. Most corporate explanations start with ownership documents. That is only half the picture. A company can change its name overnight; separating wallets, counterparties and years of operational ties is another matter when regulators can trace transactions on a public blockchain.

Customers felt the impact straight away. EXMO stopped accepting registrations and deposits. Users can no longer open trading positions, although they can still close existing ones. Why does that matter? Because trading restrictions are inconvenient, but the 29.4% of customer obligations that EXMO says it cannot repay is the real damage.

Part of the shortfall dates back to a December 2020 hot-wallet hack in which roughly 5% of EXMO’s assets were stolen. The remainder comes from money frozen by custodians and financial service providers after the May 2026 sanctions. EXMO had been using profits to cover the hack losses, but crypto prices climbed faster than the exchange could close the gap. As the affected assets became more expensive, its debt to customers grew with them. I’ll be honest: that is a brutal balance-sheet trap.

EXMO has deducted 29.4% from every client balance and issued USDRecover tokens for the amount removed. The tokens are debt claims. Customers cannot trade or withdraw them. Right now, USDRec is little more than a number in an account. The label changes nothing. Calling it a token does not make it spendable money.

The closure also shows how regulatory pressure can hurt customers who had no part in the conduct being investigated. The usual advice is to inspect an exchange’s corporate registration and stated jurisdiction. Counter to that advice, wallet relationships may reveal more than the paperwork. UK authorities appear more interested in how a business operates than in what its documents claim, and two supposedly separate exchanges sharing wallets may not look separate at all.

Investors need to know who owns an exchange and where it operates. They also need to know who controls its wallets and which outside firms can block access to the money. Crypto trading comes wrapped in the language of decentralization, yet most exchanges are conventional centralized companies. They rely on banks and payment providers; custodians add another point of failure. Any one of them may freeze funds after a government order. Regulators have already pursued much larger platforms through the SEC cases against Binance and Coinbase. EXMO is smaller, but I doubt that distinction means much to someone who just lost access to 29.4% of a balance.

After news of the EXMO sanctions broke, Bitcoin briefly tested support near $61,400 and then recovered. The move was limited. Pinning it entirely on EXMO would be a reach—and, in my view, lazy market storytelling. Traders were still alert to the possibility that enforcement could spread to other exchanges. One closure may barely move the market while the prospect of a second or third keeps everyone watching.

The wind-down lays bare the counterparty risk inside centralized exchanges. Customers now hold illiquid IOUs for almost a third of their balances. This story is painfully familiar: an exchange runs into trouble, then withdrawals slow. Only afterward do users discover that the balance on the screen was a claim against a company, not cash waiting in a vault. We know this pattern. It still catches people.

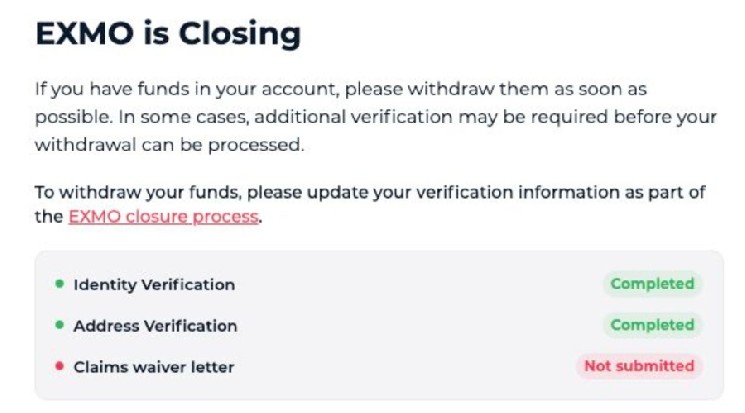

EXMO says customers can withdraw what remains of their funds, although processing will be slower than normal. Users must complete verification; some will face further identity checks. The exchange has also warned that it may convert assets under unusual liquidity and pricing conditions. Fees may rise as well. Is that a minor operational detail? Not after an automatic 29.4% deduction, when every added delay and cost stings.

Self-custody is bound to look better after this. The phrase “not your keys, not your crypto” can sound smug during quiet markets, but EXMO is exactly the sort of case that keeps it alive. Still, the standard self-custody sermon goes too far. Moving coins off an exchange does not eliminate risk; it changes who is responsible for it. Some investors may choose exchanges with clearer ownership and custody practices, while others will move more holdings into wallets they control. I would not expect a dramatic Bitcoin candle today. A gradual change in where people keep their money is more plausible.

What this means

Regulators are looking more closely at crypto companies suspected of assisting sanctioned entities. EXMO’s case suggests that UK officials will inspect wallet records and operating ties even after a company claims to have sold or separated part of its business. May 26, 2026 is the concrete warning here: formal separation did not stop EXMO Exchange Limited from landing on the sanctions list. My take is simple. Murky ownership or connections to politically sensitive markets add a layer of risk that users cannot afford to ignore.

For EXMO’s customers, policy takes a back seat to the 29.4% shortfall. Almost a third of their money is now trapped in a non-tradable IOU with no clear path back to cash. That is counterparty risk without the finance jargon. Some users may turn to self-custody or DeFi. Yes, that sounds like the obvious answer—but it is incomplete. People lose wallet keys, and smart contracts fail. Risk does not disappear. It just lands somewhere else.

In the coming months, investors should watch sanctions announcements alongside exchange disclosures about customer asset custody. Smaller and mid-sized platforms could feel the strain first if banks or custodians decide that serving them is not worth the compliance trouble. Institutional fund movements may offer another clue. To my eye, large investors pulling assets from exchanges with similar exposure would say more than a polished reassurance on a company blog.

For Bitcoin, $60,000 and $65,000 remain useful reference points as traders absorb more enforcement news, but they are hardly crystal balls. A move past either level would carry more weight if trading volume rose. Another set of sanctions against crypto firms would matter too. EXMO customers have a less abstract concern, though: they want to know whether a USDRec token will ever become a real dollar again.