In a recent development, CoinList, a well-known cryptocurrency exchange, has been ordered to pay a hefty amount of $1.2 million to the US Treasury as a settlement for violating sanctions imposed by the Office of Foreign Assets Control (OFAC).

According to OFAC’s statement, CoinList had allowed clients from Crimea to use their services, in direct violation of the sanctions. The exchange’s employees were found to have opened a total of 89 accounts for these clients, all of whom indicated Russia as their country of residence but provided postal addresses on the Crimean Peninsula.

During the period from April 2020 to May 2022, CoinList conducted financial transactions for these clients, which amounted to a staggering 989 apparent violations of the sanctions regime. As a consequence, the exchange is now obliged to pay the substantial fine.

OFAC emphasized the importance of virtual currency companies abiding by sanctions in a risk-based manner, especially when catering to a global client base.

This incident comes on the heels of ATAIX Eurasia, a licensed cryptocurrency exchange in Kazakhstan, urging Russian users to close their accounts prior to December 15, 2022. This decision was driven by EU sanctions, which now prohibit the exchange from offering its services to Russian individuals and legal entities.

In another significant development, Binance, a major cryptocurrency exchange, made the decision to completely exit the Russian market at the end of September. The exchange sold its local business to CommEX as a result.

Eleanor Ashworth is editor-in-chief at BTCNews. A Cambridge-trained journalist with 18 years across the Financial Times, Reuters and the Telegraph, she joined the crypto beat in 2017 after covering the Bank of England and HM Treasury. She holds the SABEW Best in Business award (2022) and was shortlisted for the British Journalism Awards (2023). At BTCNews she sets the editorial line for Bitcoin and macro markets coverage, with a focus on institutional adoption, regulation and central-bank policy. Based in London.

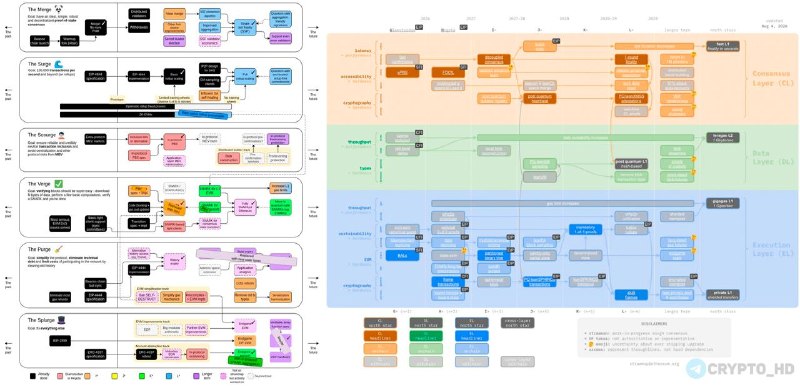

Vitalik’s Ethereum roadmap puts quantum security and privacy first

Vitalik Buterin’s revised Ethereum roadmap now treats quantum security and privacy as “first-class goals.” Why does that matter? Because institutions judging Ethereum’s durability increasingly want to know whether a blockchain built to run for decades can withstand the next generation of security threats. Quantum computers cannot break Ethereum today. No need to panic. My take: starting early is simply responsible engineering.

Buterin has reshuffled Ethereum’s development priorities. Quantum security moved up. VDFs (Verifiable Delay Functions) and most “cosmetic” EVM (Ethereum Virtual Machine) changes moved down or vanished. Verkle trees have lost favor too; the roadmap now prefers PBT, a simpler state structure that works well with ZK proofs. Most roadmaps only add ideas. This one also kills them, which may be the more important part.

Privacy is also a “first-class goal” for the protocol. The proposed toolkit includes keyed nonces and privacy pools. Wormholes and parts of FOCIL are in the mix as well. Regulators continue to scrutinize transaction transparency, yet companies and ordinary users have legitimate reasons to keep financial activity private. I’ll be honest: the idea that every onchain payment should remain permanently visible to anyone has never struck me as especially practical. Better safeguards could attract users who currently avoid public blockchains because every transaction leaves an inspectable trail.

For traders, this gives ETH a narrative beyond DeFi and NFTs. Does that mean a higher price? Not necessarily. Coins such as Monero (XMR) show that markets value anonymity, although Ethereum is not trying to remake itself as a privacy coin. Its tools could still appeal to users who want more control over what they expose onchain. I see credible demand there. A guaranteed catalyst? No.

The roadmap also explores post-quantum scaling systems such as zkzk-frames and leanSPHINCS. Quantum computers are not an immediate threat to Ethereum’s cryptography, so panic would be misplaced. Counter to the usual advice, though, waiting for an attack to become practical would be reckless. Markets price distant risks early, and long-term holders may appreciate seeing defensive work begin before the threat becomes urgent.

Ethereum’s specification is being “Lean-ified” as well. In plain English, developers want to remove enough complexity to make full formal verification with AI possible. That should make the software easier to inspect and prove correct. This part gets painfully technical. Still, when institutions put large sums into infrastructure, predictable behavior usually beats architectural cleverness. I think that trade-off is worth making.

Native rollups would become part of Ethereum itself, while blob- and gas-futures would help the network anticipate demand. Scaling remains a priority, but the approach is narrower: improve specific pressure points instead of trying to accelerate the entire system in one shot. Simpler virtual machines such as leanISA or RISC-V could eventually replace the old EVM. That is not a cosmetic refactor. It is foundational work.

Overall, the plan aims to prepare Ethereum for future quantum attacks while making it easier to verify and more private. Native rollups might also pull some activity back toward Ethereum’s base protocol. Polygon (MATIC) and other scaling networks already hold a share of that market. If Ethereum handles rollup functions itself, more value may stay inside its ecosystem. Most bullish summaries present that outcome as obvious. It isn’t; the roadmap cannot guarantee it.

What this means

The roadmap rethinks Ethereum’s architecture rather than adding another collection of minor upgrades. The Ethereum Foundation is preparing for risks that may remain distant, while privacy and scaling problems affect users now. Is that overambitious? Maybe. I find the direction encouraging, but skepticism is fair until developers ship working code.

Quantum protection and built-in privacy may appeal to institutions and governments seeking blockchain infrastructure they can rely on for years. A simpler specification could matter even more in finance and the public sector, where one obscure software bug can become extremely expensive. Yes, that sounds less exciting than a new consumer app. It may also be more valuable. ETH could benefit if the crypto market rewards steady technical progress, but a roadmap remains a plan and cannot create price gains by itself.

Investors should focus on delivery, particularly native rollups and the proposed privacy tools. Testnet launches and published specifications count. So do concrete developer updates. In my view, those signals reveal far more than another sweeping announcement. ETH’s response to major releases may then show whether traders believe the work is genuinely advancing.

Privacy regulation matters just as much. Ethereum could benefit if it satisfies users without triggering restrictions, but that balance will be difficult. The next few quarters should show whether the proposals turn into measurable network changes. Traders may also watch the $4,000 resistance level. Holding above it could indicate firmer confidence; one price level, however, would not prove that the roadmap caused the move. Correlation is not delivery.

FAQ

Q: What are the main priorities in Vitalik’s updated Ethereum roadmap?

A: Quantum security and privacy. The roadmap treats both as “first-class goals” for the protocol.

Q: How does the roadmap address quantum computing threats?

A: It explores post-quantum scaling technologies, including zkzk-frames and leanSPHINCS.

Q: What changes are planned for the Ethereum Virtual Machine (EVM)?

A: Developers may eventually replace the old EVM with simpler virtual machines such as leanISA or RISC-V.

Q: How would Ethereum improve privacy?

A: The proposals include keyed nonces and privacy pools, plus wormholes and parts of FOCIL.

Q: What would native rollups do?

A: They would bring rollups directly into Ethereum’s protocol to support scaling. Blob- and gas-futures would help the network prepare for changes in demand.

Q: What does “Lean-ification” mean here?

A: It means simplifying Ethereum’s specification so developers can formally verify it with AI. That would also make its behavior easier to check.

Q: Could the roadmap affect institutional investment in Ethereum?

A: Possibly. Institutions may value stronger privacy and early preparation for quantum attacks. Easier-to-verify software could help too. Investment will still depend on delivery, regulation, the wider market and each institution’s risk tolerance.

Q: What should investors watch?

A: Watch for native rollup releases and working privacy features. Specific development milestones matter as well, along with decisions on crypto privacy regulation.

James Whitfield is markets correspondent at BTCNews. He spent eight years on the equity desk at Bloomberg London before moving to digital assets in 2020, and now leads our daily coverage of spot prices, derivatives and ETF flows. James reads order books for breakfast and has been quoted in the Financial Times, CityAM and CoinDesk. He is a CFA Level III candidate and is based in the City of London.