Michael Saylor MicroStrategy BTC Risk Tests Corporate Bitcoin Treasuries

“Michael Saylor’s MicroStrategy Bitcoin strategy is now a direct market risk, extending beyond a mere corporate finance narrative,” Arca’s CIO said. The michael saylor microstrategy btc risk debate is not just another MSTR argument on a bad Bitcoin tape. My take: it matters because BTC holders, MSTR investors, and MicroStrategy preferred shareholders could all be exposed during the same four-month stretch. That is the uncomfortable part.

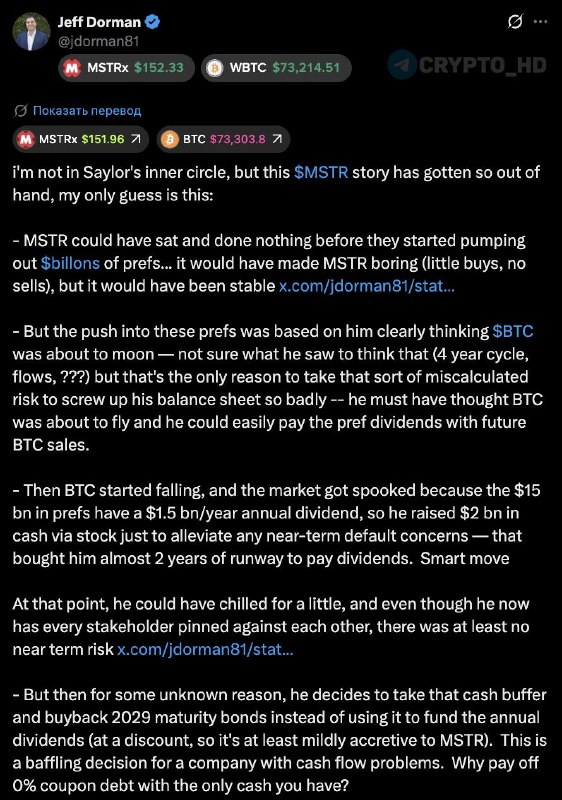

“MicroStrategy’s issuance of billions in preferred stock fundamentally altered its financial trajectory, moving it from a simple Bitcoin proxy to a complex capital-markets entity,” Arca’s CIO said, according to the source post. He is basically saying the trade got harder to read. MicroStrategy once looked cleaner: buy BTC, avoid selling, let MSTR trade as a dramatic Bitcoin proxy. Then MicroStrategy issued $15 billion in preferred shares and created about ~$1.5 billion in annual dividend obligations. That changed the object on the table. It became less “levered BTC” and more “funding machine that needs Bitcoin strength.”

“The decision to issue preferred stock appears to have been predicated on an expectation of a significant Bitcoin price surge,” the source said. That is a serious accusation. If MicroStrategy built this structure around a hard BTC rally, then a Bitcoin drawdown would not merely lower MSTR’s net asset value. It could pressure the balance sheet and dividend obligations at once. Investor confidence would get hit too. Why does this matter? Because for crypto traders, MSTR stops being only an adoption headline and starts looking like a possible source of BTC selling pressure. Not a small change.

“MicroStrategy’s role as a flagship corporate BTC treasury trade is now accompanied by significant structural vulnerabilities,” Arca’s CIO said. Most guides frame corporate Bitcoin treasuries as simple demand. That is only half right. Treasury demand is bullish only when the buyer can survive volatility without turning into supply. MicroStrategy has long been treated as the main corporate BTC treasury trade, but Arca’s CIO argues the $15 billion preferred share issuance and later ~$1.5 billion annual dividend bill made the structure more fragile. If that buyer later has to sell coins to meet obligations, adoption becomes supply risk.

“MicroStrategy subsequently raised an additional $2 billion in cash through an equity placement, providing a temporary reprieve from immediate default concerns,” the source said. MicroStrategy then raised another $2 billion in cash through an equity placement. The market read was plain enough: near term default fears eased, and the company appeared to have about two years of dividend coverage. I would not dismiss that. MSTR investors could breathe a little, BTC traders could stop pricing an immediate forced sale, and preferred holders had a clearer payment cushion. For a while, the structure looked strained but workable. It worked.

“MicroStrategy’s decision to use its cash reserve to buy back 2029 bonds, rather than preserving it for preferred dividends, raises significant questions about its financial strategy,” Arca’s CIO said. Then came the move that makes the whole setup harder to defend: MicroStrategy allegedly used that cash reserve to repurchase bonds maturing in 2029, rather than keeping it for preferred dividends. The bonds were reportedly bought back at a discount, so yes, there was a benefit. Still. A company under cash flow pressure usually does not spend available cash retiring zero coupon debt early unless it has another funding plan, another liquidity source, a strong belief that BTC will recover fast, or some mix of all three.

“MicroStrategy functions as a high-beta expression of Bitcoin, amplifying market movements in both directions,” market analysts said. The second crypto angle is flow. MSTR is not BTC. Traders still use it like a higher beta Bitcoin trade. When risk appetite improves, MSTR can magnify demand; when BTC weakens, the leverage cuts the other way. The source does not give a specific BTC price level or percentage move, so investors should not invent one. The hard numbers are already enough: $15 billion in preferred shares, ~$1.5 billion in annual dividends, $2 billion in cash raised, and a 2029 bond buyback. Those figures explain why BTC liquidity matters here.

“MicroStrategy’s financial structure intertwines Bitcoin exposure with traditional corporate finance instruments, challenging the narrative of Bitcoin as a purely independent asset,” financial commentators said. This is also a safe haven test, though not the usual geopolitical one. BTC bulls often say Bitcoin sits outside the traditional financial system. Counter to the usual advice, MSTR makes that argument messier, not stronger. It wraps BTC exposure inside corporate debt, preferred equity, common stock, and dividend obligations. If MicroStrategy ever sells BTC during a long Bitcoin drawdown, the market probably will not treat it as routine treasury management. It would look like forced selling by the most visible corporate BTC holder. That would put the “strong hands” story under real pressure.

“Despite current challenges, Michael Saylor’s historical ingenuity in capital markets suggests the possibility of an unforeseen strategic solution,” Arca’s CIO said. I will be honest: writing off Saylor’s capital markets creativity has been a bad trade before. Maybe there is a plan. One possibility in the source is that MicroStrategy could refinance its convertible bonds with later maturities, even though Saylor previously said the company was moving away from convertible debt. Is that a contradiction? Yes, partly, but it would at least explain why MicroStrategy might repurchase 2029 obligations now. It would not erase the dividend burden. It could push the liquidity problem further out.

“The most straightforward and concerning scenario involves MicroStrategy being compelled to sell its Bitcoin holdings,” the source said. The bearish case is cleaner and uglier: BTC sales. The source suggests selling Bitcoin may eventually become the company’s option, and selling during a longer BTC decline would hurt both BTC and MSTR. This part is blunt. MicroStrategy is not some unknown wallet. If the market starts to believe MSTR must sell BTC to fund preferred dividends, then every transfer and financing deal becomes tradeable information. Balance sheet updates do too. The source’s earlier note about MicroStrategy moving BTC to an exchange only makes traders more sensitive to it.

“A fundamental conflict has emerged among MSTR common shareholders, BTC holders, and preferred shareholders, who previously shared aligned interests,” Arca’s CIO said. The main conflict now sits between groups that used to want roughly the same thing. MSTR common shareholders want BTC upside and a premium equity story. BTC holders want MicroStrategy to keep buying, or at least keep holding. Preferred shareholders care about cash dividends first. Ideology comes second. Yes, this cuts against the tidy “everyone wins if BTC goes up” framing. Bear with it. Arca’s CIO argues this is the first time MSTR holders, BTC holders, and preferred shareholders are all in a tough spot at once. Someone may take real losses within the next four months.

“MicroStrategy is evolving into a critical signaling asset for Bitcoin market structure, reflecting underlying balance-sheet pressures,” market analysts said. For traders, MSTR is becoming a signal for BTC market structure. If MSTR falls faster than BTC, the market may be pricing balance sheet stress instead of simple Bitcoin beta. If BTC drops and MSTR’s preferred stock trades poorly, investors may start asking whether the ~$1.5 billion annual dividend obligation can be paid without selling coins. If Saylor announces refinancing, the pressure could ease. If he sells BTC, the pressure likely moves straight into spot Bitcoin liquidity.

What this means

“The corporate Bitcoin treasury trend is entering a more challenging phase, as evidenced by MicroStrategy’s complex financial structure,” financial commentators said. The corporate Bitcoin treasury trade looks harder now. MicroStrategy’s model worked best when BTC appreciation, equity issuance, and investor demand moved together. Now the source describes a more conflicted stack: $15 billion of preferred shares, ~$1.5 billion of annual dividends, $2 billion of cash raised, and a debt buyback tied to 2029 maturities. The affected tickers are BTC and MSTR. The affected trade is even clearer: using MSTR as a leveraged Bitcoin proxy without taking the funding stack seriously. Skip that step.

“The next four months will be crucial for observing MicroStrategy’s strategic financial decisions and their impact on both MSTR and BTC,” financial analysts said. Watch the next four months closely. The list is specific, not vibes-based: whether MicroStrategy refinances the 2029 convertible bonds, raises new capital, keeps enough cash for preferred dividends, or sells BTC. For BTC traders, price is not the only signal. MicroStrategy wallet movement, exchange transfers, and financing updates may matter just as much. For MSTR investors, the question is blunt: can the company keep the Bitcoin upside story alive while carrying a ~$1.5 billion annual dividend burden without becoming a forced seller?