Bitcoin Mining Cost Squeeze: What It Means for BTC Price Action

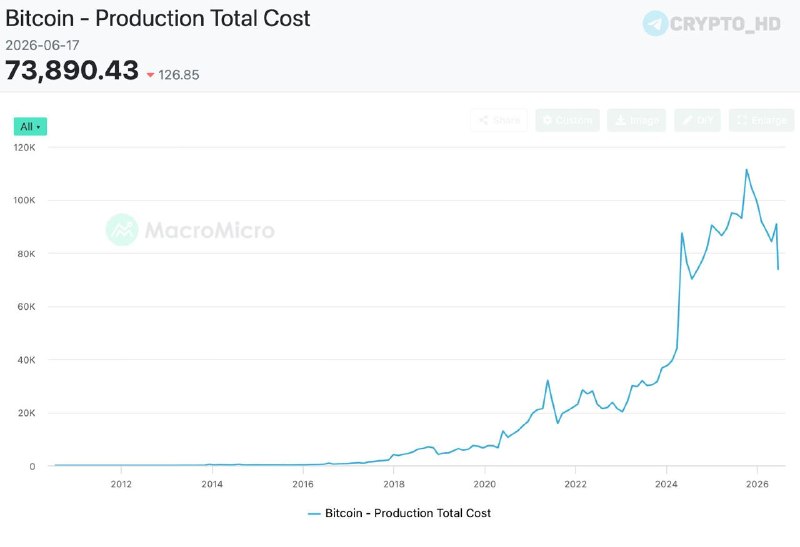

Bitcoin miners are under pressure. The average cost to mine 1 BTC is now above the spot price. MacroMicro puts the average mining cost near $74,000 per coin, while BTC trades around $62,000. JPMorgan has said BTC has traded below its estimated production cost for five months. That gap matters. Not in a vague “sentiment” way. It means some operators are producing coins at a loss, and if enough of them sell BTC just to stay online, that pressure can leak straight into price action.

The math is rough: many miners are spending more to produce BTC than they can sell it for. MacroMicro estimates that one mined Bitcoin costs about $74,000 on average, compared with a market price near $62,000. JPMorgan says the gap has lasted for five straight months. I’ll be honest: I would not treat the $74,000 figure as exact, since mining costs depend on power contracts, machine age, debt, and location. Still, the direction is hard to brush off. Roughly 20% of miners are believed to be operating at a loss. Some may need to sell BTC reserves to pay electricity bills and hosting fees. Payroll and interest do not wait either. The weakest operators usually go first. Older ASIC fleets with expensive power have very little room to stall. Efficient miners may still be fine. The middle gets squeezed.

This crunch matters for BTC because forced selling can become a steady drag on the market. Miner selling is not just a chart signal. It is supply. Why does this matter? Because miners that sell coins every week to cover costs can add pressure right when traders are already watching Fed decisions and inflation data. Risk asset flows are the other piece. Bad timing, basically. Bitcoin has been through versions of this before. In past bear markets, miner selling often appeared near painful price zones, though it did not always mark the exact bottom. Most guides imply miner capitulation is a neat bottom signal. That is only half right. During the March 2020 liquidity shock, BTC fell with equities before ripping higher. That showed both sides of the asset: it can trade like a risk asset during panic, then break away when conditions change. My take: persistent miner selling could make the next rally harder, even if macro conditions improve.

Mining stress can also make people question Bitcoin’s security and decentralization story, even if the network itself is not in danger. Spot BTC ETFs have pulled more institutional money into the market, but the mining layer still matters. If less efficient miners shut down and larger players take share, the network may look more concentrated. That does not mean Bitcoin is about to break. It does mean investors may start watching mining pool concentration more closely. This is where the story gets messier than a clean ETF inflow chart. Corporate treasuries and institutional buyers often justify BTC exposure partly through Bitcoin’s security model and decentralization. If the mining base looks narrower, even for a while, some allocators may hesitate. Is that overkill? For a short-term trade, maybe. For anyone underwriting BTC as infrastructure, no. The market will be watching hashrate and pool share, plus any sign that weaker miners are getting pushed out faster than difficulty can adjust.

What this means

The mining squeeze points to a rough consolidation phase for Bitcoin miners. Some operators will shut down, sell machines, merge, or get bought. That is painful. It may leave the sector leaner if the survivors have cheaper power and newer hardware. Better balance sheets help too. Yes, this slightly cuts against the usual “capitulation is bullish” take. Bear with me. Consolidation may improve efficiency later. Right now, the issue is simpler: miners under pressure may sell BTC, and that can weigh on price. We have seen this setup before. It gets ugly first.

Investors should watch the network data, not just the BTC chart. Hashrate and mining difficulty are the main tells. A sharp hashrate drop could mean more miners are capitulating, which may bring more price volatility. The difficulty adjustment happens every 2,016 blocks, roughly every two weeks, and it will show whether the network is starting to absorb the stress. Counter to the usual advice, I would not only stare at ETF flows here. Also watch MacroMicro’s production cost estimate, the $62,000 BTC area, and the $74,000 mining cost level. A sustained move below $62,000 would keep pressure on weaker miners. A recovery above $74,000 would put more of the industry back in profit and could reduce forced selling. Simple levels. Big consequences.