India Telegram ban over exam leaks: a regulatory warning for crypto

India’s week-long Telegram ban over exam question leaks says something blunt about digital power: a government can still reach for the off switch fast. My take: crypto teams should not treat this as a weird messaging-app one-off. The ban hit more than 150 million users, not only the people accused of sharing leaked papers. If authorities are willing to block Telegram over misuse by a small group, wallets, exchanges, crypto apps, or protocols with large user bases can face the same kind of pressure.

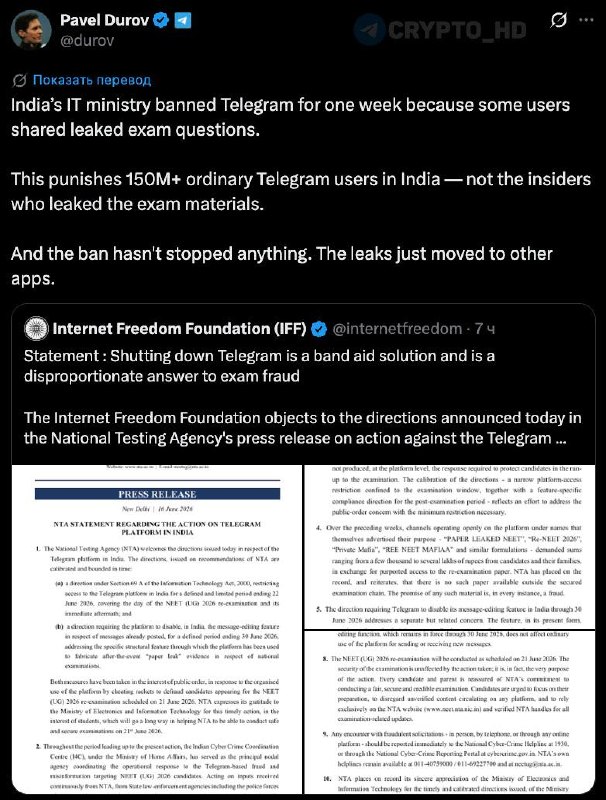

The episode began when Telegram was temporarily blocked in India. Pavel Durov, Telegram’s founder, mocked the decision in public. Officials said the block was about exam question leaks. Fair enough, exam fraud is real. But the fix landed on everyone using the app, which is where the argument starts to wobble. Durov’s point was not subtle: if exam answers are shared on Telegram, banning Telegram across the country is a strange repair job. The Internet Freedom Foundation called it a “crude ‘plaster'” on a deeper problem, not a serious attack on exam fraud. And then the obvious happened. The leaks moved to other apps. It failed fast.

This may look like a Telegram story. It is not. It matters for crypto, especially around regulation pressure, because governments are still trying to force crypto systems into rulebooks built for older financial and communications rails. India has already been a tense market on that front. Counter to the usual advice, the risk here is not only “bad regulation.” The sharper risk is blunt platform control after regulators decide a service is causing trouble. The U.S. has its own version of this, visible in the SEC’s stance on staking and the CFTC’s approach to DeFi. If a government can block a communications platform because some users posted illegal content, what stops it from restricting a decentralized exchange or protocol because some users moved illicit funds through it? Not much, honestly. The code may be neutral. Regulators may still go after app stores, front ends, domains, payment ramps, custodians, and founder teams. Crypto teams should take that seriously. It could hurt projects like TON, which is closely tied to Telegram and relies on Telegram’s reach to bring Web3 tools to regular users. Even a temporary threat to Telegram can shake confidence in TON-linked assets. Markets hate fog.

The ban also feeds into the safe-haven argument, but not in the lazy “Bitcoin fixes everything” way. This was not a banking collapse or a currency crisis. Still, blocking access for 150 million users over a platform dispute shows how fragile digital access can be. Why does this matter? Because censorship resistant tools stop sounding theoretical when a mainstream app can disappear by order. In countries where governments control information flow or limit online rights, Bitcoin and permissionless networks become easier to explain. Bitcoin has drawn interest during capital controls, inflation shocks, and periods when people want to move value outside normal channels. This Telegram ban did not send BTC ripping higher, and nobody should pretend it did. But it does make self custody feel less like crypto ideology and more like basic redundancy. If a centralized app can vanish from your phone because officials dislike how some people used it, users may start asking what else can vanish. Access to Telegram was restricted until June 22, 2026, and Telegram must disable message editing for Indian users by June 30. Those dates make this feel less like a quick warning and more like ongoing control.

Durov said Telegram is a “force for good” and called even a temporary ban a mistake. He also said Telegram had removed hundreds of channels spreading exam leaks and related scams in India in the weeks before the block. That detail matters more than it first appears. The company was already acting, but the government still chose the broadest tool available. I’ll be honest: I do not read that as a small procedural dispute. I read it as a preference for visible control over slower, narrower enforcement.

What this means

Digital platforms can become political targets fast. For crypto, the lesson is simple and uncomfortable: centralized chokepoints are still weak spots. Most guides say decentralization is the answer. That’s only half right. Users still touch crypto through websites, wallets, Telegram bots, exchanges, bridges, DNS records, mobile stores, and banking rails. India was willing to block Telegram even after the platform said it had removed hundreds of leak-related channels. That suggests a low tolerance for digital disorder, especially when public exams and national institutions are involved. Crypto investors should treat that as a real risk in large markets where regulation is still unsettled. Projects tied to decentralized communication, identity, payments, or politically sensitive user bases need to think harder about what happens when a government decides access itself is the problem. The restriction lasting until June 22, 2026, plus the June 30 message-editing demand, points to a continuing push rather than a one-time fight.

India still has huge crypto adoption potential. That is exactly why this matters. Is this overreading one Telegram fight? Maybe. But the concrete signals are hard to ignore: more than 150 million affected users, hundreds of channels already removed, access restricted until June 22, 2026, and a June 30 demand aimed at message editing itself. Any new move against digital assets, exchanges, wallets, or messaging-linked crypto products could ripple beyond India. Watch crypto bills and enforcement actions. Watch platform restrictions too. Tokens tied to decentralized communication may move first. TON is the obvious one because of its Telegram connection. MATIC could also draw attention because of its Indian roots. Yes, this sounds broader than a Telegram ban. That is the point. If the market reads this as part of a wider turn toward tighter digital controls, BTC and ETH sentiment could take a hit too. The next date to watch is June 30, when Telegram is required to disable message editing for Indian users. That may show whether this stops with Telegram or becomes a template for other platforms.

FAQ: India Telegram ban and crypto implications

- Q: What was the main reason for the Telegram ban in India?

- A: Officials said the ban was meant to stop exam question leaks.

- Q: How many users were affected by the Telegram ban in India?

- A: More than 150 million users were affected by the temporary ban.

- Q: Did the Telegram ban stop exam leaks?

- A: No, according to the Internet Freedom Foundation. The leaks moved to other apps.

- Q: How does this ban connect to crypto regulation?

- A: It shows that a government may restrict a whole platform instead of targeting specific bad actors. In crypto, that same logic could hit decentralized exchanges, protocols, app front ends, or wallet access points accused of enabling illegal activity.

- Q: Why does June 22, 2026, matter?

- A: Telegram access was restricted until June 22, 2026, which makes the measure look more serious than a brief outage.

- Q: Why does June 30 matter?

- A: By June 30, Telegram must disable message editing for Indian users. That could point to more platform-level demands from regulators.

- Q: How could this affect confidence in crypto projects?

- A: It could increase volatility for tokens tied to Telegram, especially TON, if investors start worrying about Telegram’s regulatory risk.

- Q: Does this strengthen the case for decentralized technology?

- A: Yes. If users cannot count on centralized platforms staying available, self custody and permissionless protocols become more appealing.

- Q: What did Telegram do before the ban?

- A: Pavel Durov said Telegram had removed hundreds of channels spreading exam leaks and related scams in India.

- Q: What should crypto investors watch next in India?

- A: Watch crypto legislation, enforcement moves, platform restrictions, and tokens tied to decentralized communication or major emerging markets.