Moscow Cash Dollar Euro Shortage Puts Bitcoin Hedge Trade Back in Focus

The Moscow cash dollar euro shortage is a small stress signal. Not a crisis. Exchange offices in Moscow are running low on physical dollars and euros because more people want to buy than sell. No lines. No obvious panic, according to the source. Still, buying cash FX has become difficult even below $10,000, and I think crypto investors should treat that as useful market weather. When people look for hard currency, they usually start with dollars in hand. Then the next question comes fast: what else can sit outside local money and local banks? That is where BTC and USDT reenter the picture.

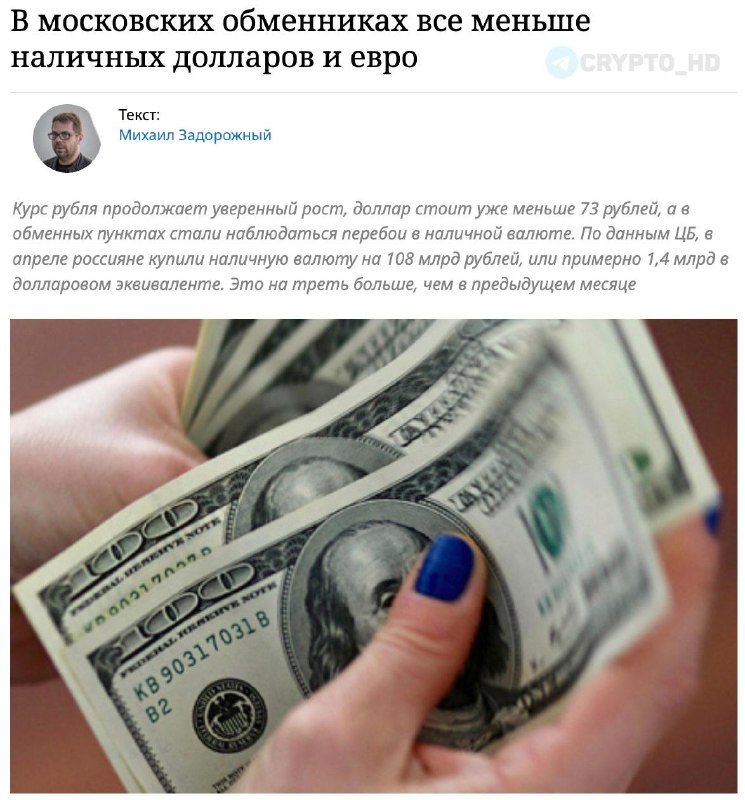

The setup is not complicated. Moscow exchange offices say they can usually buy foreign currency from customers, but they can only sell dollars or euros when someone has recently brought some in. Central Bank data cited in the source says Russians bought 108 billion rubles of cash foreign currency in April, about one third more than in the previous month. Why does this matter? Because that is not abstract “sentiment”; it is people turning rubles into physical cash. The reasons are ordinary enough: summer travel, a cheaper dollar, plus the old habit of keeping part of your savings somewhere no app login can freeze.

The first crypto angle is the hedge trade. I would be careful with it. Most guides jump from “cash dollar shortage” to “Bitcoin bid.” That is only half right. This does not mean Russians are suddenly piling into BTC because one exchange booth ran out of euros. The source does not say that. But the pattern is recognizable: when people want physical dollars, they are usually trying to reduce exposure to the local currency and the local banking system. BTC is still the cleanest liquid market test of that instinct. USDT is often what people actually reach for first, especially where getting dollars through normal channels is slow, costly, or just annoying. My take: the stablecoin leg is less glamorous, but probably more practical. For context, not as a source claim, BTC rose 8% during the January 2020 Soleimani strike. Political stress can bring the Bitcoin hedge story back quickly, even when the trade fades later.

Still, BTC is not cash in a wallet. That matters more than Bitcoin bulls like to admit. Physical dollars and euros solve blunt problems: travel, emergency savings. Payments outside domestic systems too, but that is a separate use case. BTC solves a different problem: censorship resistance and cross border settlement. ETH sits further out on the risk curve and usually trades more like a liquidity asset than a household safety asset. So the cleaner read is not “cash FX shortage equals BTC rally.” It is this: if dollar and euro cash stays hard to get, BTC and stablecoins may get a stronger narrative bid as investors price in local banking friction.

The second angle is macro flow. A cheaper dollar is one reason given for April’s 108 billion rubles of cash FX demand, and that matters because the dollar often sets the tone for crypto. When the dollar weakens, global liquidity tends to feel looser. BTC and ETH usually prefer that to dollar spikes. But this Moscow story is not simple risk on buying. It is bargain hunting mixed with caution. Yes, that sounds contradictory. It is. People can buy cash dollars because they look cheap and still be acting defensively. That mix can support cash dollars and BTC at the same time. The real test is whether this stays a travel season blip or becomes a broader savings habit.

Stablecoins sit in the middle. No surprise there. The source names dollars and euros, not USDT or USDC, so there is no direct stablecoin adoption claim to make. Even so, the signal is hard to ignore. If consumers cannot reliably buy physical dollars below $10,000, digital dollar substitutes matter more for the next layer of demand. Is this overreading one Moscow report? Maybe, if it ends here. But if the same pattern shows up in more cash desks, USDT becomes the utility trade while BTC gets the big sovereign hedge headline. COIN, as a listed exchange stock, is more of a U.S. sentiment proxy than a direct Russia trade.

There is no quote in the source, and that matters. I will be blunt: this is where bad crypto analysis usually runs off the road. The facts are narrow: Moscow exchange offices are short of cash dollars and euros; there are no queues or obvious rush; April cash FX purchases reached 108 billion rubles, about one third above the prior month. Everything after that is market interpretation. Good traders keep those buckets separate. Bad ones turn every shortage into a theory of everything.

What this means

This looks like defensive saving, not a currency panic. The important pieces are higher April demand, tighter supply, and reports that even purchases below $10,000 have become difficult. For crypto, BTC is the ticker most exposed to the story. USDT is the one to watch for actual dollar demand. Counter to the usual advice, I would not start with the Bitcoin chart here. Start with whether similar reports spread beyond Moscow, or whether the shortage continues after the vacation explanation starts to look thin. If that happens, the hedge trade gets easier to believe.

Watch the next Central Bank cash foreign currency data for May, BTC’s reaction around major macro dates such as the next FOMC decision, and CME BTC futures positioning to see whether offshore traders care. A clean BTC break through a major technical level would say more than the Moscow anecdote on its own. For now, this is a yellow light for FX stress. It is also a reminder that dollar scarcity still gives crypto one of its strongest stories.