Coinbase CEO Financial System Future Ties Crypto to Market Plumbing

The coinbase ceo financial system future roadmap says crypto is moving beyond trading. My take: that is the whole point, not a side note. The bet is larger than another exchange cycle: use crypto rails to rebuild market infrastructure through tokenized assets, stablecoin payments, AI risk checks, and the old Bitcoin argument that hard money still matters.

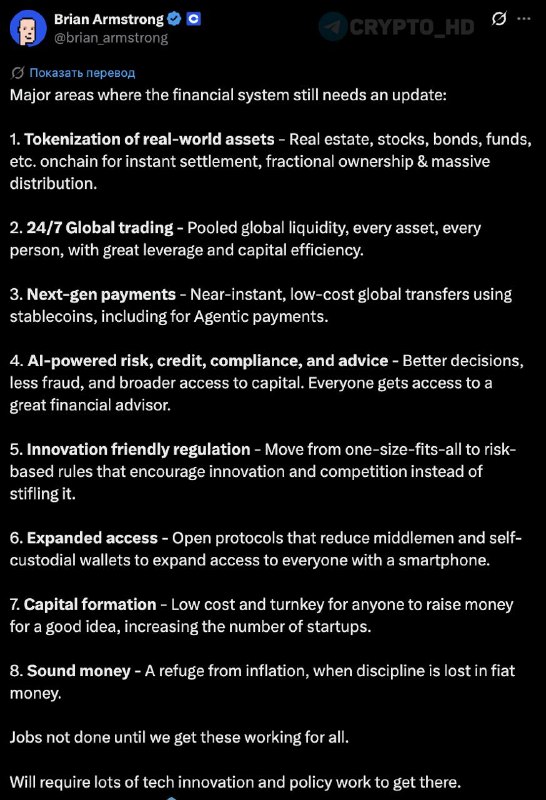

In the Coinbase CEO’s wire/TG post, the list is not tidy. It runs through tokenized real-world assets and 24/7 global trading. Then it jumps to faster stablecoin payments, AI for risk and compliance, regulation that still allows new products, open protocols, non-custodial wallets, new fundraising models, and “hard money” as protection against inflation. Messy list. Useful signal.

Yes, it reads like an adoption pitch. That is only half the story. It is also Coinbase telling investors what kind of company it wants to become. If real estate, stocks, bonds, and funds move on-chain, smart contract networks like ETH get a cleaner institutional use case. Coinbase (COIN) gets a chance at a market larger than retail spot trading.

The 24/7 trading point is blunt. BTC and ETH already trade around the clock. Traditional equities do not. Why does this matter? Because if traditional assets move toward one global liquidity pool, crypto exchanges and tokenized asset venues stop looking like side markets and start looking like actual market plumbing. COIN benefits if it can connect regulated finance to on-chain rails.

The macro angle is the other big piece. I’ll be honest: this is the part some investors will dismiss too quickly. The Coinbase CEO’s “hard money” reference is about inflation and weaker trust in fiat currencies, which is the basic BTC investment case. In that view, BTC is a balance sheet hedge against monetary debasement when investors worry that cash will lose value because of rate cuts, fiscal deficits, or inflation.

Stablecoin payments are the more practical bridge. Less dramatic. Probably more important soon. The post describes nearly instant, low cost transfers, including payments made by AI agents. For ETH, Base, and other settlement layers, that matters because payment volume can create network demand even when users are not trading.

Regulation is the third pressure point, although “third” undersells it. Counter to the usual advice, the key issue is not just whether rules are friendly or hostile. It is whether rules are specific enough for listed assets, staking products, tokenized securities, and stablecoin services to exist inside the United States instead of drifting offshore. A friendlier rulebook could give COIN more room. A harsher one could push the same activity offshore. Crypto has seen that movie before.

The AI section is smaller, but it points at credit. The post says AI can improve risk assessment, lending, and compliance, with less fraud and wider access to capital. That links open protocols with underwriting. Plainly: on-chain credit could reach borrowers who do not fit neatly inside the old banking system. Is that overclaiming? Maybe in the short run. Not in the architecture.

Financial access is the most crypto-native part of the roadmap. With open protocols and non-custodial wallets, someone with a smartphone can reach payments and savings. Trading and capital markets can sit on top of that. I would not call this new; it is the original crypto promise with better packaging. That supports the self-custody case for BTC and the app-layer case for ETH and stablecoin networks.

The capital raising point matters too. The Coinbase CEO frames crypto rails as a way to make startup formation and investment access easier for promising ideas, but with more institutional guardrails than the last cycle had. Risk based regulation, compliance AI, and tokenized ownership could make future fundraising more credible, especially if investors can check assets and disclosures on-chain. We tried the no-guardrails version already. It broke.

“The work will not be finished until all these elements work together.”

That line carries the post. Most guides separate tokenization from regulation, stablecoins from payments, and AI from compliance. That is cleaner. It is also only half right. Crypto does not become useful financial infrastructure just because one piece works. Tokenization, regulation, stablecoins, compliance, AI credit, open wallets, hard money, and payment rails have to connect. Otherwise it stays fragmented, and crypto has already burned plenty of time there.

What this means

Coinbase wants investors to see crypto as financial infrastructure, not only as a speculative asset class or a source of exchange volume. The tickers in focus are BTC, ETH, and COIN. BTC carries the hard money argument. ETH gets the tokenization and settlement demand story. COIN is the regulated access point for trading, custody, stablecoins, and tokenized assets. My read: COIN is the most operationally exposed of the three.

The next checks are specific. BTC’s reaction to the June 17, 2026 FOMC decision will matter. So will ETH demand from tokenized asset and stablecoin settlement flows, CME futures positioning for institutional BTC exposure, and COIN’s ability to turn the financial system upgrade story into products people can actually buy or use. For traders, the watchlist is simple: BTC support and resistance on daily charts. Then ETH gas, L2 activity, and COIN volume after regulatory or tokenization announcements.