Ondo Finance DTCC partnership points to wider institutional crypto adoption

Ondo Finance’s reported work with DTCC on asset tokenization looks like a serious move toward institutional crypto use. Not the loud version. The plumbing version. My take: this is where institutional crypto usually gets real before the market notices.

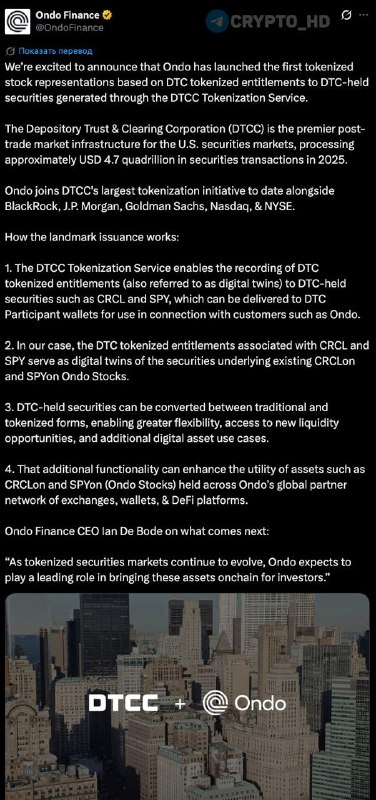

Reports say Ondo Finance has joined DTCC’s asset tokenization initiative, alongside names like BlackRock, JPMorgan, Goldman Sachs, Nasdaq, and NYSE. Ondo has reportedly issued the first tokenized share representations based on DTC tokenized entitlements through the DTCC Tokenization Service. DTCC said it processed about $4.7 quadrillion in transactions in 2025. That number is almost too large to think with, but it tells you where this sits: not on the edge of finance, but inside custody, clearing, and settlement for a large part of the U.S. securities market.

Why does this matter? Because this is not a small fintech running a side experiment with a press release attached. It involves the financial infrastructure most investors never see, even though it sits underneath their trades every day. BlackRock and JPMorgan testing tokenized assets is one thing. DTCC building services around them is different. Most crypto commentary treats those as the same category. That’s only half right.

The spot Bitcoin ETFs approved in January 2024 are a useful comparison, but not a perfect one. BTC moved above $45,000 around that time and later traded above $73,000 in March 2024, according to CoinMarketCap data. I would be careful here: that does not mean tokenized securities will trigger the same kind of move. It means institutions are getting more comfortable putting traditional assets into on-chain formats. Smaller claim. Better claim.

The capital-flow angle is the part to watch. Tokenized securities blur the line between TradFi and DeFi in a practical way, not just as conference talk. Investors want yield. They want faster settlement. They also want fewer operational headaches, cleaner transfers, and access that does not depend on old market hours. Fractional access can help when it solves a real problem. It works.

I’ll be honest: I would not assume ETH or SOL jumps just because Ondo is working with DTCC. That is too easy. Counter to the usual advice, the first winners may not be the most obvious layer-1 tokens. If even a small slice of DTCC-processed assets becomes available on-chain, demand could show up elsewhere: stablecoins, settlement rails, custody tools, compliance systems. Protocols built around real-world assets may benefit too, but only if the activity leaves the demo stage.

What this means

The Ondo Finance DTCC partnership suggests institutional blockchain work is leaving the lab and entering financial market infrastructure. That is the part worth watching. Crypto people have said for years that blockchains can make finance faster and more accessible. Yes, this sounds like the same old pitch. It is not, at least not entirely, because DTCC already sits inside the existing system instead of trying to replace it from the outside.

Is the immediate market impact going to be loud? Probably not. I would not expect every DeFi token to move at once, and frankly that would be a bad signal if it happened on headlines alone. But Ondo is now harder to ignore in the real-world asset category, which analysts at firms such as Messari and CoinGecko have called one of crypto’s bigger growth areas. It also suggests regulators may be more comfortable with tokenized securities when established firms are involved, though the rules are still far from settled.

Crypto investors should watch what DTCC tokenizes next and how much volume runs through the service. The asset quality matters too. Are these meaningful instruments, or just small test cases dressed up as progress? Announcements from BlackRock, JPMorgan, Goldman Sachs, Nasdaq, or NYSE would matter more if they involve live products instead of vague pilot language.

RWA-focused protocols and their tokens are worth tracking, but with some skepticism. The market often prices the story before the revenue exists. We have seen this pattern before in crypto: infrastructure narrative first, usage later, disappointment somewhere in between. Regulation matters too, because tokenized securities will only scale if issuers, brokers, custodians, and exchanges know what they can legally do.

Since the original 2024-2025 watch window has passed, the better question in 2026 is simple: has DTCC’s service moved from announcement to repeatable use? That is the test. Not vibes. Not logos on a slide. Repeatable use.

FAQ

Q: What is the significance of the Ondo Finance DTCC partnership?

A: It puts Ondo Finance in a tokenization effort tied to DTCC, one of the main infrastructure providers behind U.S. securities markets. My read: that makes it more serious than a standalone crypto pilot.

Q: How does this partnership impact the crypto market?

A: It gives blockchain-based finance more institutional credibility and could bring traditional assets closer to digital asset rails.

Q: What is DTCC’s role in this initiative?

A: DTCC provides market infrastructure for custody, clearing, and settlement. Here, it is supporting tokenized versions of traditional assets.

Q: What are tokenized representations of shares?

A: They are blockchain-based representations tied to traditional shares or entitlements. Think market records in token form, not magic new equity.

Q: Will this partnership directly affect crypto prices like ETH or SOL?

A: Not necessarily. Any price impact would likely depend on real usage, liquidity, and which blockchains or settlement systems are used.

Q: What are Real-World Assets (RWAs) in this context?

A: RWAs are traditional assets, such as company shares, bonds, funds, or real estate interests, represented on a blockchain.

Q: How does this partnership relate to institutional interest in crypto?

A: It shows institutions are still testing blockchain for market infrastructure, not just buying Bitcoin or launching ETFs.

Q: What should investors monitor regarding this development?

A: Watch DTCC tokenization volumes, asset types, institutional announcements, and whether RWA protocols gain real users instead of just market attention.

Q: What is the potential long-term impact on global finance?

A: If tokenized assets scale, more traditional securities could trade, settle, or move across blockchain-based systems. That would be a real change, but it will take time.

Q: Is this partnership a sign of regulatory acceptance for tokenized securities?

A: It suggests regulators may be more comfortable when established firms are involved. It is not the same as full regulatory clarity.