mastercard chainlink crypto payments reheat onchain adoption trade

Mastercard and Chainlink are back in the crypto access conversation, this time around direct onchain buying for bank card users. The headline is doing real work because 3,500,000,000 bank card holders can buy crypto directly onchain through an integration first announced in 2025. That is the hook. For traders, the mastercard chainlink crypto payments story matters because it connects a familiar card network to XSwap and Uniswap execution. My take: this is not cleanly a new catalyst. It reads more like a renewed promo cycle around an older integration. That difference matters.

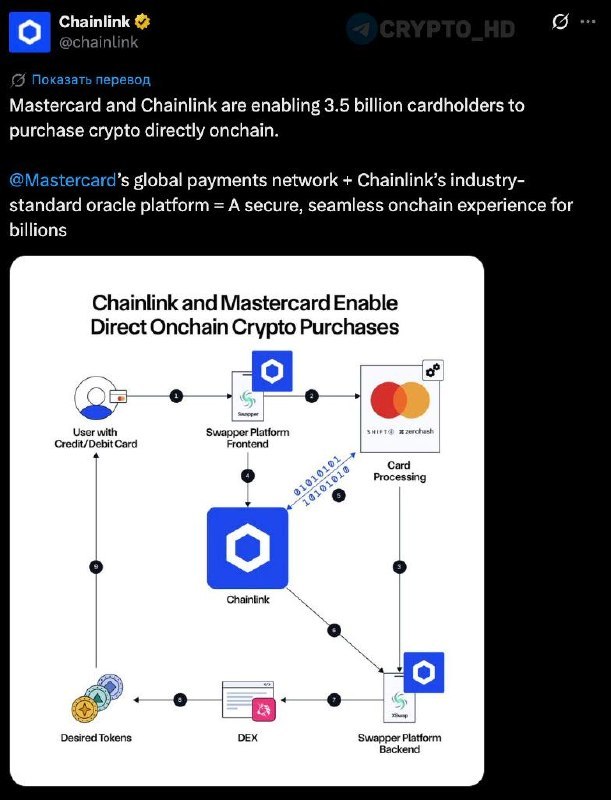

The Mastercard-Chainlink payment route has several steps between the card swipe and the onchain trade. The source post, published on twitter, lays out the route. A user pays with a regular bank card. Shift4 processes the card payment. zerohash handles fiat-crypto infrastructure, compliance, and liquidity. Swapper Finance is the interface. XSwap and Uniswap execute the onchain trade and buy the token. Small but important detail: the source says this is not a fresh partnership announcement. It is a repeat warm-up of an integration already announced in 2025.

The market signal is about Mastercard’s scale, Chainlink’s crypto reputation, and Uniswap’s role as the execution venue. There is an adoption signal here, but it needs a sober read. Mastercard brings the number everyone will screenshot: 3,500,000,000 card holders. Chainlink brings the infrastructure reputation. Uniswap brings the venue. Why does this matter? Because LINK traders need more than a big-name payment stack; they need actual onchain volume. The source gives no LINK price, no BTC price, no ETH price, no percentage move, and no dollar volume. Any claim about an immediate price reaction would be analysis, not a sourced fact.

Crypto investors have seen payment brand headlines get attention before they show up in the data. I would not overcomplicate this part. Crypto has seen this movie before. Big payment brand integrations often move attention before they move fundamentals. Most guides treat that as automatically bullish. That’s only half right. It can be useful and still be early, vague, or hard to trade. If card funded onchain buying through Swapper Finance, XSwap, and Uniswap actually grows, that would matter more for LINK, UNI, ETH, and stablecoin rails than the social media repost. The market usually buys the story first and checks the receipts later.

The main crypto angle is adoption: direct token access inside familiar card infrastructure. The first crypto angle is adoption. Mastercard and Chainlink appearing in the same payment flow tells investors that card infrastructure is still moving toward direct token access, not just custodial crypto balances inside fintech apps. The source’s main number is 3,500,000,000 card holders. The date to keep in mind is 2025, because the source says the integration was already announced then. The tickers in view are LINK for Chainlink exposure, UNI for Uniswap exposure, and ETH because Uniswap activity still sends traders back to Ethereum liquidity when execution happens onchain.

The adoption angle is not automatically bullish, especially if this is a reheated 2025 story. This is not a straight line bullish setup. I’ll be honest: I would be slower to chase this than the headline suggests. Traders should watch whether LINK acts like an infrastructure proxy or fades because the post is mostly a reminder. A fresh Mastercard-Chainlink announcement in 2026 would say one thing. A renewed push around a 2025 integration says something else: marketing pressure and ecosystem positioning. Also a reminder that card-to-onchain conversion is still a live fight. The source makes that distinction. The market should, too.

The second crypto angle is macro flow: easier card access widens the funnel, but risk appetite decides what comes through it. Card-to-crypto access gives more people a path into BTC, ETH, LINK, and UNI. That does not mean they will take it. In a high-rate or sticky-inflation market, investors may respect the infrastructure progress and still refuse to add risk. Is this overkill for a payment headline? No, because the June 16-17, 2026 FOMC meeting sits right in the path of liquidity-sensitive crypto trades. Traders should watch whether payment integration headlines survive rates volatility. It can happen fast.

BTC and ETH often trade like liquidity assets, so macro pressure can drown out easier buying access. Context, not a new source fact: BTC and ETH often behave like high-beta liquidity assets when the market is focused on Federal Reserve policy, real yields, and the U.S. dollar. That matters here. Easier buying access does not cancel macro pressure. Counter to the usual advice, the cleaner payment route may not matter first. BTC may matter first. If BTC is breaking higher into June 16-17, 2026, adoption headlines can add fuel. If BTC is losing a major support level into that same window, LINK and UNI may struggle even with a cleaner payment story.

There is also a regulation angle because someone has to handle compliance between fiat, liquidity, and onchain execution. The source does not cite the SEC, CFTC, or any legal filing, so this should not be dressed up as a regulatory development. Still, the compliance piece is worth watching. According to the source, zerohash handles fiat-crypto infrastructure, compliance, and liquidity. In 2026, investors care less about whether a bank card can technically touch a token and more about who carries the compliance risk between the card payment and the onchain trade. For COIN, centralized exchanges, and regulated onramps, the question is blunt: does card-to-onchain buying steal flow from exchange accounts, or does it expand the market?

Zerohash’s compliance and liquidity role lets Swapper Finance keep the front end simple while XSwap and Uniswap handle execution. This is where zerohash becomes more than background plumbing. If compliance and liquidity sit behind the interface, Swapper Finance can feel simple to the user while XSwap and Uniswap do the onchain work. For traders, the stack is easy to map: LINK for the oracle and infrastructure story, UNI for decentralized exchange exposure, ETH as the base layer liquidity proxy, and BTC as the benchmark risk asset. The source gives no token-specific percentage move. Watch attention first. Then volume.

The repost is the signal, and it appears meant to remind the market about the full Mastercard-Chainlink payment chain. The source gives no reaction quote, so inventing one would weaken the piece. The better read is that the repost itself is the signal. Someone wants the market to remember that Mastercard, Chainlink, Shift4, zerohash, Swapper Finance, XSwap, and Uniswap are all part of the same payment route. My read: that is positioning before fresh volume data, not proof that fresh volume already exists. It also means traders should be careful about treating the post like a new catalyst when the source says the announcement dates back to 2025.

For the main tokens, the trading questions are about relative strength, visible onchain flow, transaction demand, and a wider investor base. For LINK, the clean question is whether renewed Mastercard attention creates relative strength against BTC and ETH. Not whether the story sounds impressive. For UNI, watch whether execution through Uniswap becomes visible in onchain flow. For ETH, ask whether more user-facing payment routes create transaction demand or stay stuck as integration talk. For BTC, the link is broader. If traditional payment rails normalize token buying, the reachable investor base grows beyond crypto-native exchanges.

The payment chain has several dependencies, and each one can add friction. This is not a retail onboarding fairy tale. Every step adds a dependency: Shift4 for card processing, zerohash for fiat-crypto infrastructure, compliance, and liquidity, Swapper Finance for the interface, and XSwap plus Uniswap for execution. More partners can mean more reach. They can also mean higher fees, jurisdiction limits, user drop-off, and operational breakpoints. The source does not provide fee data, supported tokens, countries, or transaction limits. So no, the 3,500,000,000 card holder figure is not proof of universal access.

The bullish case is that ordinary card users get another path into onchain markets without opening a traditional exchange account. The bullish case is easy to understand. If even a small slice of ordinary card users can move from fiat into tokens without opening a traditional exchange account, onchain markets get another distribution channel. That helps the adoption case for LINK, UNI, and ETH. The skeptical case is just as easy. A 2025 integration getting warmed up again in 2026 may create social attention without proving new demand. Both can be true in the same week. Crypto does that a lot.

What this means

This points to deeper crypto access inside payment infrastructure, but it is a reminder of a 2025 integration rather than a new Mastercard-Chainlink deal. The market should treat this as a reminder of an existing 2025 integration, not a newly announced Mastercard-Chainlink partnership. The tickers to watch are LINK for Chainlink, UNI for Uniswap, ETH for onchain execution activity, and BTC as the risk appetite benchmark. The source gives 3,500,000,000 card holders, but no price level, no percentage move, and no volume figure. My take: the first real confirmation has to come from market behavior and onchain flow, not the headline by itself.

Traders should watch LINK/BTC, LINK/ETH, UNI volume, and Uniswap activity around the June 16-17, 2026 FOMC meeting. LINK/BTC, LINK/ETH, UNI volume, and Uniswap activity are the cleaner tells around the June 16-17, 2026 FOMC meeting. Macro flow can either help this story or smother it. Yes, that sounds like it contradicts the adoption angle above. It does not. Adoption can improve while the trade still fails. If BTC and ETH hold key support into that date, the Mastercard-Chainlink payment narrative has a better shot at pulling in risk capital. If rates volatility hits crypto first, this may trade like another familiar integration repost: useful as a longer term signal, thin as a short term catalyst.