JPMorgan, Mastercard and Ripple Just Pushed Tokenized US Bonds Onto a Public Chain

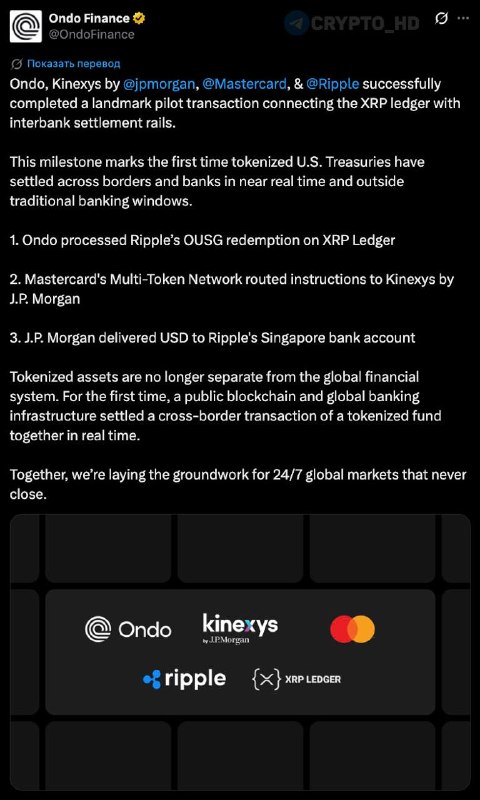

Here is what actually happened. JPMorgan’s Kinexys arm, Mastercard, Ondo Finance and Ripple closed a cross-border deal in tokenized US Treasury bonds that ran across the XRP Ledger and traditional banking rails. One money-center bank, one global card network, one tokenization shop, one public blockchain. Same ticket. That is the part I keep circling back to. Twelve months ago that lineup did not exist on a single transaction. My take: for crypto markets, this reads less like headline noise and more like an adoption signal with direct read-throughs to XRP, RLUSD and the broader real-world-asset thesis.

The mechanics are why it matters. Kinexys is JPMorgan’s blockchain payments arm, and the bank says it has been moving large institutional volumes on-chain for some time. Mastercard handled the multi-rail settlement layer. Ondo brought the tokenized US government bond through OUSG, which is on-chain exposure to short-duration Treasuries. Ripple closed the loop by routing settlement through the XRP Ledger, the public chain tied to its institutional payments push and to RLUSD. Four logos. One transaction. Public-chain involvement was not a footnote. Most guides still frame bank blockchain work as private-ledger experimentation. That is only half right.

The adoption read is concrete because the XRP Ledger now has a branded institutional use case. XRP has spent most of the past two years clawing back credibility after the SEC litigation cycle. A live cross-border bond settlement involving JPMorgan and Mastercard is the kind of validation Ripple has been chasing. Tokenized asset trackers like RWA.xyz already show tokenized US Treasury products as one of the largest real-world-asset categories on public chains, with Ondo, BlackRock’s BUIDL and Franklin Templeton’s BENJI fighting for share. Why does this matter? Because if the XRP Ledger settles into a regular rail for tokenized treasury flow, demand shifts from narrative-driven XRP bursts toward actual ledger activity.

Tokenized treasuries are the cleanest bridge between TradFi yield and crypto-native capital. Stablecoin issuers, DAOs, on-chain funds and treasury desks can park idle dollar liquidity in tokenized T-bill products to grab short-duration government yield without leaving the chain. I’ll be honest: the yield story is useful, but it is not the real prize. Every new institutional rail that goes live opens a compliant path for sidelined capital. JPMorgan’s own commentary on blockchain settlement keeps returning to regulated cash movement, counterparty controls and integration with existing treasury systems. JPMorgan sitting at the settlement layer matters more than another retail-facing token launch. Bank-grade compliance is what eventually unlocks pension, insurance and corporate treasury money downstream.

The regulatory subtext is the more interesting part. Big banks are getting visibly more comfortable testing tokenized government debt on blockchain infrastructure. JPMorgan is the highest-profile skeptic-turned-builder in this whole market. Jamie Dimon has trashed Bitcoin in public for years while Kinexys quietly grew the bank’s blockchain payments business. Mastercard touching a public-chain transaction is also a tell, because card networks have historically preferred controlled or permissioned environments for regulated settlement pilots. Counter to the usual advice, the key detail is not just “institutional partners.” It is that this deal ran on the XRP Ledger, a public and permissionless chain, not just a closed ledger. The regulatory comfort line is moving. Tokenized government debt on public infrastructure is now a working test case for the SEC, the OCC and overseas regulators trying to draft the next round of digital asset rules.

The announcement has real limits, and traders should be honest about them. No transaction size was disclosed. No settlement window was disclosed. There is no clarity on whether RLUSD acted as the cash leg or whether the dollar leg ran through Mastercard’s traditional rails. That ambiguity is normal for a first-of-kind pilot. Still, it is the gap I would not paper over before pricing this as a fully productionized settlement flow. Is this overkill? No, because right now it is a pilot, not a confirmed recurring protocol.

The competitive read is that Ondo just bagged a high-value institutional proof point in tokenized treasuries. Its involvement nudges it ahead of BlackRock’s BUIDL on the cross-border settlement use case, even though BUIDL is still bigger by AUM. For Ripple, this is one of the strongest institutional proof points since RLUSD launched. Yes, this sounds like the opposite of the caution above. Bear with me. A pilot can be commercially limited and still strategically important. BIS and McKinsey research on cross-border payments puts corporate and wholesale flows in the multi-trillion-dollar annual range. That is the prize Ripple is actually aiming for if stablecoin-settled and tokenized-asset flows graduate from pilots into recurring infrastructure.

What this means

This is an institutional proof point for tokenized treasuries, the XRP Ledger and real-world-asset infrastructure. It also reframes what tokenized treasuries are for. The retail framing, “earn T-bill yield on-chain,” is quietly being replaced by an institutional framing where tokenized bonds become settlement collateral for cross-border corporate flow. That shift drags the addressable market out of crypto-native land and into multinational corporates that already wire dollars through correspondent banks. XRP gets the most direct read-through, because its ledger now has a live, branded use case backed by a top-five US bank and a top-two card network. RLUSD’s positioning as an institutional stablecoin gets practical support, not just marketing copy. Ondo strengthens its position in the tokenized RWA category against BUIDL and BENJI.

The next few data points will decide whether this becomes infrastructure or stays a one-off. First, watch whether JPMorgan, Mastercard or Ripple discloses transaction volume or signs up for repeat settlements. A one-off pilot is a press release. A recurring flow is infrastructure. Second, watch XRP and ONDO price action plus XRP Ledger transaction volume over the next 30 days. I would weight ledger activity more heavily than spot price here. Real institutional adoption usually shows up in usage before it shows up cleanly in the chart. Third, watch the next SEC or OCC comment on tokenized treasury settlement. A permissive posture could unlock the next big wave of tokenized treasury inflows. A tighter line on public-chain settlement could push competing flow back onto permissioned rails. The rail is live now. The question now is who lines up behind it.

FAQ

What did JPMorgan, Mastercard, Ripple and Ondo Finance settle? A cross-border transaction in tokenized US Treasury bond exposure that ran across traditional banking infrastructure and XRP Ledger-linked blockchain rails.

Why does this matter for XRP? The deal hands the XRP Ledger a branded institutional use case involving JPMorgan, Mastercard, Ripple and Ondo. If similar flows recur, ledger activity could see real settlement demand instead of speculative volume.

What role did Ondo Finance play? Ondo provided the tokenized US government bond exposure through OUSG, its on-chain short-duration Treasury product.

Did RLUSD settle the cash leg? The announcement does not say. That detail still matters for assessing how central RLUSD really was to the transaction.

Is this a full production launch? No. No recurring production flow has been disclosed. Based on what is public, treat it as a pilot until repeat volume or operating details show up.

Why are tokenized US Treasuries important? They let blockchain users hold short-duration government yield without moving assets off-chain. Real-world-asset market trackers already rank tokenized Treasury products among the largest institutional RWA categories in crypto.

What should investors watch next? Disclosed transaction volumes, repeat settlements, XRP Ledger activity, ONDO performance, XRP price action, and any regulatory comments from agencies like the SEC or OCC.