Circle Arc Token Presale Lands $222M from BlackRock, Apollo, a16z at $3B FDV

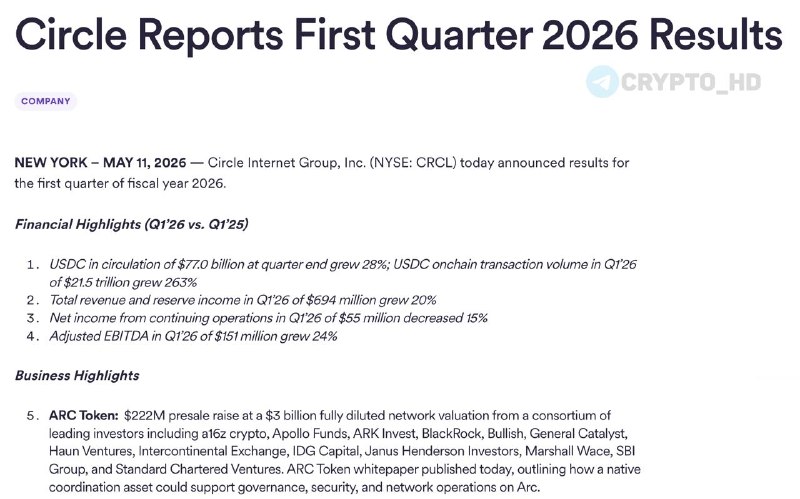

Circle just closed a $222 million private round for its Arc token at a $3 billion fully diluted valuation. The buyers: BlackRock, Apollo, a16z crypto, ARK Invest, ICE, and Standard Chartered Ventures. A Sunday report says Circle pulled the capital into the native token of its Arc Layer-1 network, and the cap table does not read like a normal crypto raise. It reads like Wall Street picked seats before the doors opened. My take: for a stablecoin issuer launching its own L1, this is barely “funding.” It is a regulatory and distribution moat being assembled in public.

The round fits Circle’s earlier plan to ship a native token on Arc, the chain it pitched for stablecoin settlement and institutional rails. $3B FDV puts Arc beside real settlement-layer projects, not experimental side quests. Not a side bet. Also, this is presale money. These funds bought before public price discovery, which usually means they expect the listing to clear $3B, not merely touch it.

The investor list is the actual story here. BlackRock runs BUIDL on Ethereum and issues IBIT, the spot Bitcoin ETF holding north of $50B AUM per their own disclosures. Apollo has been moving private credit on-chain through tokenized funds. ICE owns the New York Stock Exchange. Standard Chartered is one of the few global banks that publishes constructive BTC and ETH research with a straight face. Put those names in one Arc round and the signal is not subtle. TradFi wants a stablecoin-native chain it can underwrite. Circle just sold them equity in the plumbing.

On adoption, I’d call this the cleanest institutional vote stablecoins have gotten since Circle’s NYSE listing as CRCL earlier this cycle. USDC supply is near record highs. Every dollar that settles on Arc instead of Ethereum or Solana is fee revenue those L1s do not get. ETH holders, pay attention. Current on-chain data shows roughly $180B in stablecoin transaction settlement routing through Ethereum. Why does this matter? Because even a 10–15% capture by Arc would show up in ETH burn and validator economics. That is not theory. That is the thesis keeping ETH above $3,000 through this cycle’s chop.

Regulation is where this gets sharper. Most guides will say the token structure is the key issue. That’s only half right. The buyer list matters just as much. ICE and Standard Chartered Ventures don’t usually back tokens that look legally brittle, and their presence implies Circle has structured Arc’s tokenomics and the ARC token to survive SEC scrutiny, probably as a utility or network fee token rather than a profit-sharing instrument. If Arc gets a green light and Solana’s SOL or other L1 tokens don’t, mandate-bound capital has an obvious place to rotate. Coinbase (COIN), which custodies a fair chunk of institutional crypto, sits in the middle of that flow either way.

There’s a macro layer worth flagging too. BlackRock and Apollo aren’t crypto-native funds chasing 100x. Their own investor materials say they allocate against rate cycles and institutional risk frameworks. I’ll be honest: that makes this round more interesting, not less. Two of the largest asset managers on the planet are writing nine-figure tickets into a stablecoin-native L1 while the Fed is still in higher-for-longer mode. That tells you where they think real-yield tokenized assets are going. Stablecoins are the on-ramp. Arc wants to be the highway. If that highway carries tokenized treasuries, private credit, payment flows, and exchange settlement at scale, demand for the ARC token compounds with every new RWA product launched on the chain.

One thing the source doesn’t say, and I think it’s worth being upfront: the presale price per token, the public listing date, and the vesting terms for these strategic investors are all still unpublished. Until Circle drops a real token economics paper, $3B FDV is a headline number, not a level you can trade. Retail searching how to buy Circle Arc token won’t have a venue yet. Is this overkill to stress? No. Secondary markets usually open weeks to months after a raise this size, and early access tends to route through Coinbase or Circle’s own channels first.

The other quiet detail: this round closed the same week several majors were pushing hard on US stablecoin legislation. Timing at this size is rarely an accident. Yes, that sounds conspiratorial. It is also how institutional crypto launches usually work.

What this means

The takeaway: the biggest pools of TradFi capital have stopped asking whether stablecoins belong on bank-owned rails. They’ve started buying equity in crypto-native rails instead. That is bullish for the structural USDC thesis, and by extension for CRCL the equity. It is messier for ETH and SOL. Both lose mindshare to a chain built specifically to undercut them on stablecoin throughput, even if neither loses dominant share overnight. BTC sits adjacent to all of this. Institutional comfort with a Circle-issued L1 deepens the broader case for crypto as an asset class, which historically lifts BTC on a 60–90 day lag.

Three signals to watch over the next quarter. First, Circle’s official token economics release. That will show whether ARC has genuinely captive demand or is just another fee-extraction token dressed up nicely. Second, the public listing venue and date. If Coinbase lists first, expect a CRCL and COIN sympathy move on the announcement. Third, USDC’s share of monthly stablecoin transfer volume versus USDT. Current Artemis and DefiLlama tracking suggests Arc’s launch should accelerate USDC’s gains if the chain ships as advertised. Counter to the usual advice, I would not watch price first here. Watch disclosure. If those pieces line up, $3B FDV at presale will look like the floor by year-end. If Circle stumbles on timing or token details, $3B becomes the ceiling fast.