Grayscale’s Quarterly Reshuffle: What the New DeFi and Smart Contract Lineup Actually Tells You

Every quarter, Grayscale Investments rewrites the guest list on its sector funds. Some tokens get added. Some get cut. Weights move back toward the market-cap rulebook the firm publishes ahead of time. This time, the useful signal sits in two places: the DeFi Fund and the Smart Contract Fund. My take: this is not just portfolio housekeeping. When the largest US crypto asset manager rewrites its index, billions in passive money eventually follows, and traders treat the reset as a rough read on which corners of crypto institutional capital still considers serious.

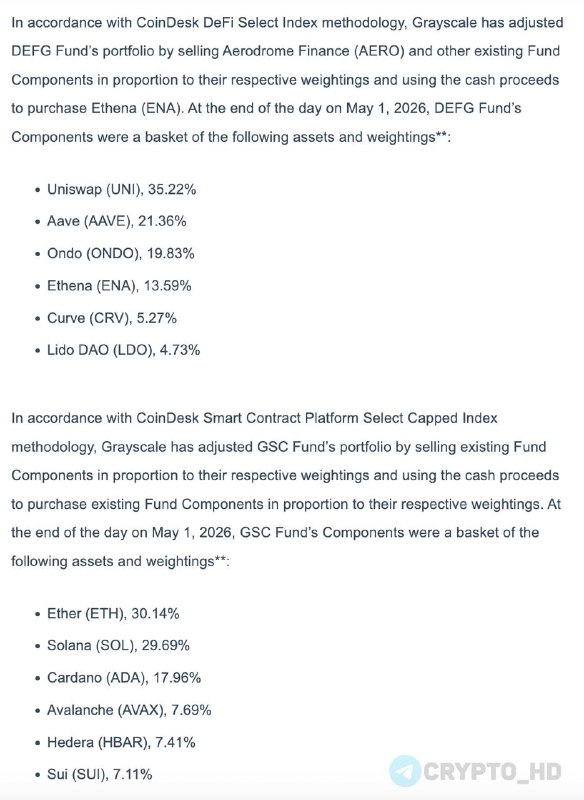

The confirmed moves are simple: one purchase, one sale, plus a refreshed list of names on the books. The DeFi Fund tracks decentralized finance protocols. The Smart Contract Fund holds layer-1 platforms that compete with Ethereum. Per Grayscale’s published methodology, both funds rebalance on a calendar cadence so weights stay tied to the underlying market-cap framework. Short version: the math runs first.

Here is the part most people miss. Grayscale is not just any holder. This is the same shop behind GBTC and ETHE, the trusts that traded at deep NAV discounts for years before flipping to spot ETFs in 2024. I’ll be honest: the smaller sector funds are where the quiet tells show up. A token kept in the lineup has not merely survived price action; it has cleared liquidity, custody, and internal risk filters again. The bar is high: custodial readiness and regulatory comfort, plus minimum daily volume. Getting cut is often less about price than about plumbing.

The macro context makes the signal louder, although not in the clean way people want. The timing lands in a market still chewing through Fed positioning and ETF flow data. BTC has spent the last several months trading like a hybrid risk asset, rallying on rate-cut hopes and fading on hawkish surprises. Why does this matter? Because sector funds like these tend to magnify the same impulse. When institutional money rotates from BTC into alts, smart-contract baskets can outrun spot ETH. When risk comes off, they usually bleed faster. A rebalance event resets the leverage points inside that beta, which is why anyone watching ETH/BTC or the alt-season index should treat this update as a cue, not a footnote.

Most guides frame inclusion as bullish and removal as bearish. That is only half right. Every name kept in the basket is, in effect, a vote of institutional confidence; every name removed carries both a downgrade signal and a mechanical flow problem. Removals tend to drain liquidity for weeks afterward because index-tracking flows unwind first. That asymmetry is why on-chain desks watch Grayscale rebalances so closely. The fund itself is modest next to the spot BTC ETF complex, but the read-through to tier-1 exchanges, custody desks, and structured-product issuers is real. If a token is good enough for a Grayscale sector fund, it is good enough for a wealth-management slot. If it is not, those slots quietly close.

History rhymes here. Grayscale trimmed constituents in earlier 2024 and 2025 cycles, and the pattern repeated each time. Winners compounded. Dropped names underperformed for at least a quarter. We tried to treat that as coincidence at first; the flow mechanics make that hard to defend. It is not a guarantee, no. But the tendency is documented enough to matter: forced selling on removal, mechanical buying on addition, then discretionary capital following the path the indexers just marked. The quarterly rebalance is both a snapshot and a forcing function.

The regulation angle is quieter, but it is there. Counter to the usual advice, I would not read the lineup only as a market-cap screen. Every constituent in a registered product passes a securities-law screen. Per public filings and prior Grayscale disclosures, the firm has been careful since the SEC’s 2023 enforcement waves, and its lineup tends to track which tokens are sitting on safer regulatory ground. Is that a perfect legal map? No. But watching what stays and what goes inside these two funds is a free read on how a heavyweight US issuer interprets the current legal climate around DeFi protocols and L1 tokens. The read is more conservative than what crypto-native funds run. It is also more durable.

The rebalance also resets downstream reference data, which sounds dull until money starts moving. It updates the public-facing holdings page. That page then becomes the reference document for separately managed accounts, retail wrappers, structured notes, and benchmark-aware portfolio sleeves that key off Grayscale baskets. Those vehicles do not all move on day one. They move in the days and weeks after, as portfolio managers true up to the new weights. That delayed flow is what creates the post-rebalance drift disciplined traders try to front-run. Small delay. Real impact.

What this means

The reshuffle is best read as a directional signal about institutional appetite inside two specific buckets: DeFi protocols and smart-contract layer-1s. Yes, this contradicts the neat “rebalance equals trade signal” framing above. Bear with me. The real read is simpler and slower: any name kept on the balance has cleared an institutional gate one more time, while any name removed faces mechanical selling pressure plus a confidence hit. The DeFi Fund and Smart Contract Fund are not the largest pools in crypto, but they shape allocation decisions well beyond their AUM, because wealth managers and structured-product desks treat Grayscale’s lineup as a working shortlist.

My watch list is narrow. First, the next NAV print and any disclosed weight shifts on Grayscale’s holdings page; that is where the new composition becomes tradable information. Second, ETH/BTC, plus the spread between the Smart Contract Fund’s underlyings and ETH itself. If the basket starts outperforming spot ETH, that points to institutional rotation rather than noise. Third, the next Grayscale rebalance window. Per the firm’s stated cadence, these run on a quarterly schedule, so the current update sets the baseline for the next read. Liquidity desks should also keep an eye on volume in any token added or removed for at least ten trading sessions, since that is the typical window for index-driven flow to clear.