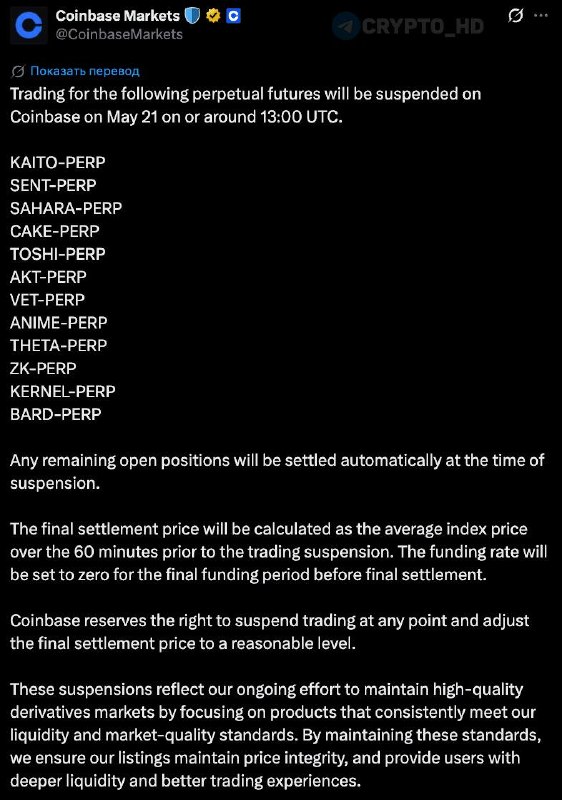

Coinbase Delists Futures Contracts on 12 Pairs Starting May 21

Coinbase is pulling 12 perpetual futures contracts on May 21, 2026. Small notice. Real consequences. If you trade altcoin leverage on the second-largest U.S. exchange, this is not just housekeeping. The notice gives the basics: a dozen perp pairs, one settlement window, no explanation. I’ll be honest: the silence is the part I notice first. Futures volume is where price discovery actually happens for most altcoins right now, not spot. Why does this matter? Because when a top-tier U.S. venue prunes its list, liquidity gets redistributed, funding rates wobble, and anyone holding open interest on those pairs has under two weeks to unwind or roll out.

Coinbase confirmed the date and the affected contracts. They did not say why. Exchanges almost never do, which is convenient for them and annoying for everyone else. Futures delistings usually trace back to low average daily volume or thin order books. Sometimes it is regulatory heat on a specific token. Sometimes it is the dullest answer: a product cleanup because the contracts never earned their keep. Most guides over-focus on the reason. That’s only half right. The operational fallout is the same either way: after May 21, anyone who wanted leveraged exposure to those names through Coinbase has to move to Binance, Bybit, OKX, or stick to spot.

That migration is the first thing I would track. The U.S. derivatives footprint has been a sore point for domestic traders ever since CFTC enforcement actions reshaped what onshore venues can offer. Public CFTC records show the pattern clearly enough: when a U.S.-licensed venue trims its futures menu, open interest leaks offshore. CME hangs onto its institutional BTC and ETH contracts. Coinbase hangs onto its flagship perps. The long tail of altcoin leverage drifts to Binance, Bybit, and OKX, where U.S. customers, on paper, are not supposed to be trading. My take: that drift quietly weakens the regulatory argument that domestic venues can absorb the demand.

The second angle is regulator pressure on the exchanges themselves. Coinbase operates under a settlement framework with U.S. regulators that scrutinizes its product listings and marketing, per its prior SEC and CFTC disclosures. Pulling twelve futures contracts at once is not a vacuum decision. It points to an internal compliance review, a quiet reaction to a regulator inquiry, a flat commercial call that those markets were not earning their seat, or some messy blend of all three. Yes, this sounds like speculation. It is. But the shareholder question is concrete: COIN investors watching derivatives revenue have to ask whether this trims a meaningful slice of the company’s quarterly mix.

Thin futures markets fail in predictable ways in the final days before a delisting. Funding rates spike as positions get force-closed. Basis widens against spot, then liquidations cluster where liquidity is worst. If you have open interest on any of the twelve pairs, the boring answer is the right one: close before May 18 to dodge the last-week chop. Skip the drama. The more interesting question is what happens to spot prices on those tokens once the leverage venue disappears. Academic work on futures market closures suggests that removing a futures market reduces price volatility on the underlying asset over the following month, because the speculative tail gets cut off. Lower volatility tends to drag volume down. Prices often follow.

For the broader crypto market, this is not a Bitcoin-moving event. BTC and ETH perps are safe, and Coinbase’s flagship derivatives keep trading. Counter to the usual “crypto is getting more institutional” storyline, though, this is a contraction in the exact product category where short-term price action gets manufactured. Spot ETF flows dominate the headlines. Derivatives move the tape. A smaller onshore derivatives surface means less of that action happens under U.S. compliance rules.

What this means

The delisting itself is narrow. The trend it fits into is not. Two indicators are worth watching after May 21. First, look for Binance or Bybit listing the same twelve pairs in the days after the cutoff. That would be the cleanest tell that volume is migrating offshore rather than dying. Second, listen to COIN’s next earnings call for commentary on derivatives revenue mix. Per Coinbase management’s prior shareholder letters, futures growth was flagged as a key 2026 lever. Trimming the product list cuts directly against that messaging. Is this over-reading one notice? Maybe. But in derivatives, product removals often say more than product launches.

For traders, the calendar is short. Positions on the twelve affected contracts should be unwound or rolled to a different venue before the final settlement window. After May 21, expect a few noisy days on those tokens as forced-close liquidity hits the order books, then a quieter regime as speculative leverage exits the system. We have seen this pattern before in exchange cleanups: first the scramble, then the silence. The bigger question for the next quarter is whether this is a one-off cleanup or the start of a longer pruning cycle at U.S.-licensed exchanges. The next CFTC enforcement headline will probably answer that for us.