JPMorgan: Bitcoin Over Gold as Middle East Conflict Drives Debasement Trade

JPMorgan sees a rotation from gold into bitcoin as the preferred debasement hedge. Three straight months of net inflows into spot bitcoin ETFs, while gold ETFs keep bleeding from the March drawdown. The bank’s latest capital flows research does not really dance around it. Money is moving into bitcoin over gold as the hedge of choice against Middle East fallout, and the tape backs that up. Bitcoin spot ETFs have logged net inflows for a third month running. Gold ETFs are still underwater from March. My take: for traders watching BTC’s correlation regime flip in real time, that gap is the whole story of the quarter. Maybe not the cleanest story. But the one that matters.

The “debasement trade” is a portfolio play. Buy gold or bitcoin to insulate against fiat erosion, sticky inflation, and geopolitical risk. JPMorgan calls it a debasement trade rotation. Fine. That phrase sounds colder than the trade actually feels when macro desks start repricing war risk and fiscal risk at the same time. The basic idea is simple: own gold or bitcoin when fiat starts looking less sturdy. What’s new is the destination. When the latest round of conflict broke out in the Middle East, the reflex bid that historically went to bullion did not show up the same way. A meaningful slice went to bitcoin instead. Worth noting, this is JPMorgan saying it. Not a crypto-native shop talking its own book.

The flow data confirms the shift. Spot bitcoin ETFs have absorbed three consecutive months of net creations. Gold ETFs have failed to repair the March outflow gap. The flow data is the cleanest evidence this cycle. Three straight months of positive net creations into spot bitcoin products is not a one-week headline trade. It is a slow drip. Gold ETFs, by contrast, never repaired the March gap. Institutions did not return in size. Retail did not chase. Why does this matter? Because allocators notice asymmetry before they rewrite mandates. BTC funds quietly absorbing capital while gold funds sit underwater on monthly flow is exactly the kind of pattern that gets pulled into the next investment committee deck.

The rotation is structural, not event-driven. Two pieces of market plumbing prove it. The spot ETF wrapper and CME futures open interest, with retail and institutional demand layered together. Most guides would stop at “bitcoin is becoming a safe haven.” That’s only half right. Yes, Middle East tensions cracked the door. The harder question is why the rotation stuck after the initial headline impulse faded. Two pieces of plumbing answer that. First, the spot ETF wrapper finally gave traditional advisors a compliant way to express the trade without custody friction. Second, CME futures open interest tells you institutions are layering exposure on top of cash positions, not just dabbling. Retail comes in through IBIT and friends. The pros stack basis trades at the CME, and some add outright longs. Same direction, different machinery.

JPMorgan says the dual-track demand turns the safe-haven argument from slogan into measurable signal. Flows survived the initial geopolitical news cycle and kept compounding. That dual-track demand is what turns the safe-haven argument from a slogan into something measurable. A pure war-bid would spike and fade inside a week. This did not. JPMorgan is describing flows that survived the initial geopolitical news cycle and kept compounding. I’ll be honest: gold’s failure to absorb that capital is starting to read less like a temporary preference and more like a generational handoff. Strong claim, yes. The flow tape is making it easier to defend.

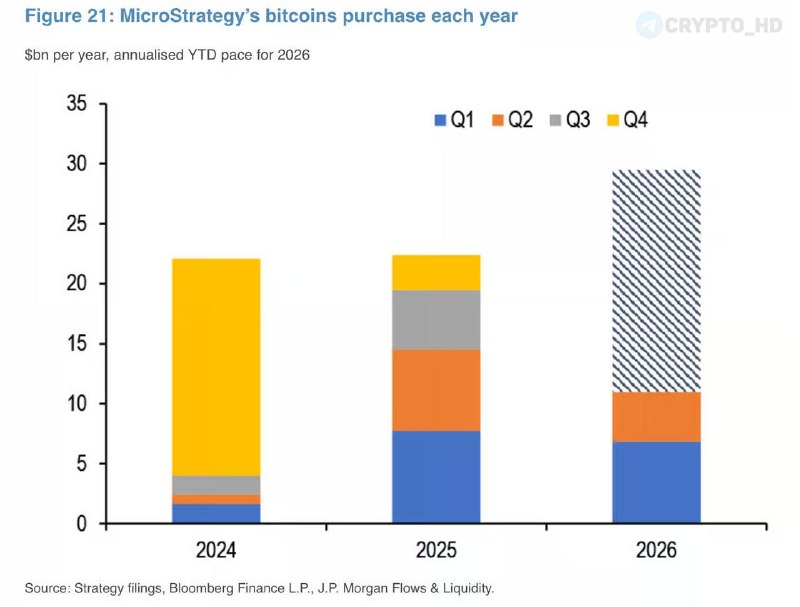

Strategy, Michael Saylor’s vehicle formerly known as MicroStrategy, is still the largest corporate bitcoin holder globally. It is on pace for roughly $30 billion in BTC purchases through 2026. Then there is the corporate channel. This is where the adoption signal gets loud. Strategy has not just kept buying this year. It has accelerated. If the current cadence holds through year-end, the company’s 2026 BTC purchases could land somewhere around $30 billion. That is not a treasury allocation. That is balance-sheet conviction at a scale most public companies will never approach.

Three simultaneous flow buckets are pulling bitcoin supply off the market in parallel. ETF retail, CME institutional, and Strategy corporate. Gold has no equivalent demand structure. Stack the flow buckets together, but do not make it too neat. ETF retail is one channel. CME institutional demand is another. Strategy corporate buying sits outside both and pulls supply in a different way. Gold has no equivalent to a Strategy. There is no S&P 500 component levering its balance sheet to buy bullion every quarter. The bid behind BTC right now has no real parallel in the metals complex. That is the part of the JPMorgan note that should matter most to anyone modeling the next twelve months.

Debasement trades historically ignite ahead of fiscal crises, not in response to them. Current positioning is anticipatory, not reactive. Here is the awkward bit. Debasement trades tend to ignite when the fiscal narrative gets ugly, not when it is already broken. The fact that real money is rotating now, before any acute fiat crisis, points to positioning ahead of an expected impulse rather than a reaction to one. Counter to the usual advice, allocators do not always wait for confirmation. They front-run the thesis their own research desks are already publishing. That is how cycles stretch.

Three months of ETF inflows during choppy spot price action signals long-horizon allocation by registered investment advisors and family offices. Not short-term speculative tourism. The retail-versus-institutional split inside the ETF complex matters too. Three months of inflows during choppy spot price action is the tell. Cleaner uptrends pull in tourists. Sideways tape with persistent net creations points to somebody with a longer time horizon loading exposure. In my view, that somebody is increasingly registered investment advisors and family offices using the spot products as their first-ever direct BTC exposure. Once that allocation lands in a model portfolio, it tends to stay. It sticks.

The cash-and-carry trade is long spot ETF, short CME futures. It locks in funding spreads while tightening bitcoin’s effective float, because the long leg is held in custody rather than circulated on exchange. The CME story rhymes, but it is more technical. Futures open interest growth alongside ETF inflows is the signature of basis arbitrage mixed with directional-long demand, not pure speculation. When CME OI rises during ETF inflows, cash-and-carry desks can go long spot ETF, short CME futures, and lock in the funding spread. Is this overkill as an explanation? No, because the mechanic changes float. The long leg is held in custody rather than flipped on exchange, so the trade soaks up additional spot demand while tightening bitcoin’s effective supply.

The destination of the rotated capital is what disproves the simple “gold profit-taking” counter-narrative. Money went into bitcoin, not cash, T-bills, or short-duration credit. Skeptics will say gold has had its moment in 2026 and that any rotation is just profit-taking from a stretched bullion position. Fair point on entry. But it is not enough. If this were merely gold consolidating, the rotation would more naturally land in cash, T-bills, or short-duration credit. It went specifically into a competing scarcity asset that JPMorgan itself is calling out by name. Yes, this slightly contradicts the tidy “safe-haven” framing from earlier. Bear with me. The destination of the capital is the proof.

What this means

JPMorgan’s endorsement of bitcoin over gold gives allocators the institutional cover they were waiting for. Expect formal mandate revisions, with directional implications for BTC, spot ETFs (IBIT, FBTC), and equity proxies like MSTR. JPMorgan calling bitcoin a better debasement hedge than gold is the kind of mainstream cover that can turn allocator hesitation into mandate revisions. Read it as a directional signal for BTC against the broader risk-off complex, not a tactical call. The tickers most directly leveraged to this rotation are BTC itself, the spot ETF lineup, including IBIT and FBTC, plus equity proxies like MSTR through Strategy’s accelerating buys. If the bank’s thesis plays out, the same rotation that punished gold ETFs in March keeps starving them through summer while BTC products absorb the difference.

Four watch-list signals will confirm whether the rotation is structural. Monthly ETF flow prints, CME open interest and basis spread, Strategy’s 8-K disclosures, and bitcoin’s behavior into a Middle East ceasefire. Watch list for the next leg. First, monthly ETF flow prints. A fourth consecutive month of net creations would confirm the rotation is structural rather than situational. Second, CME bitcoin futures open interest and the basis spread. A widening basis with rising OI says the institutional side is leaning in harder. Third, Strategy’s next 8-K disclosure on BTC purchases. Any acceleration toward the implied $30 billion annual pace puts a hard floor under spot supply. Fourth, the Middle East ceasefire tape. What if tensions de-escalate and BTC inflows hold anyway? Then the safe-haven bid has probably graduated from event-driven to structural. Crypto investors who built the bitcoin-over-gold thesis on intuition now have JPMorgan’s flow data doing the heavy lifting. The question for the rest of 2026 is no longer whether the rotation is real. It is how long gold’s allocators wait before they capitulate to it.